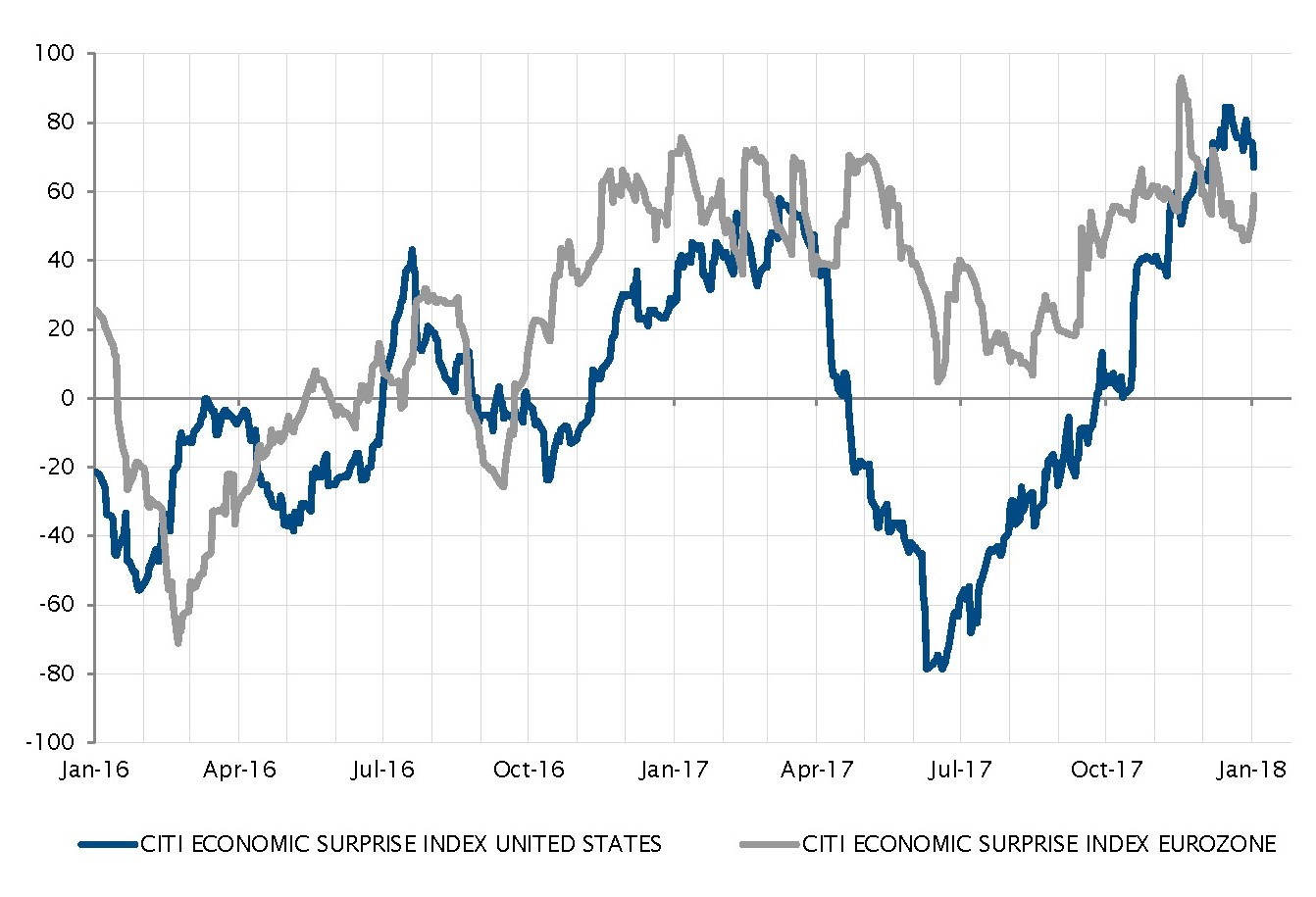

The economic and financial backdrop hasn’t changed much over the last few weeks. And it won’t just because we have entered a new year: a goldilocks environment, coupled with stretched valuations, still prevails. The only noticeable economic news has been the US tax reforms and related cash repatriation. This will lift growth temporarily and add about $10 to S&P500 EPS or about 7% additional earnings growth this year to a rough consensus estimated average of $150. How the repatriated cash will be split between M&A, exceptional dividends and productive investment, remains an open question depending on specific stocks and sectors but, again, this boost should not alter the economic outlook beyond 2018.

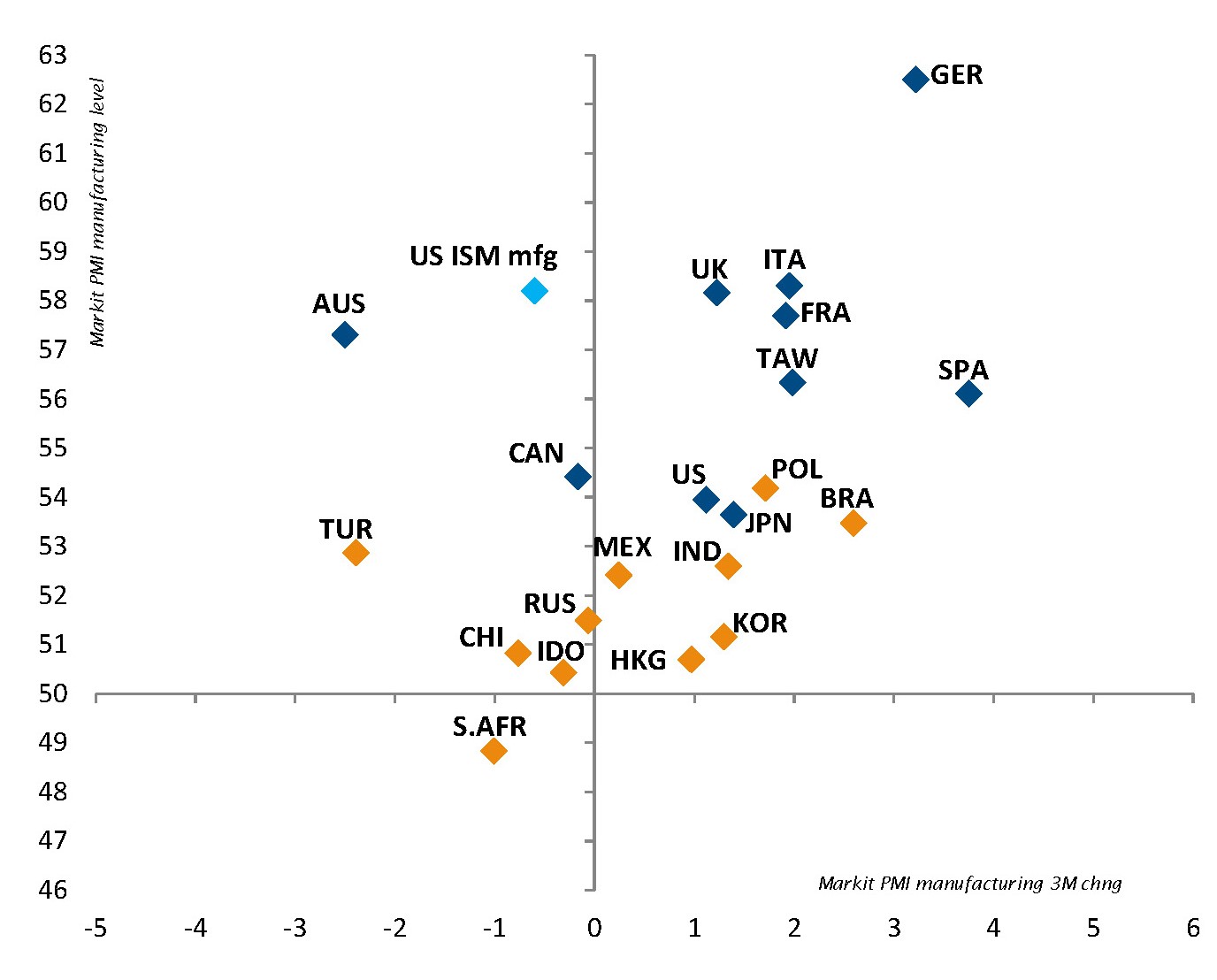

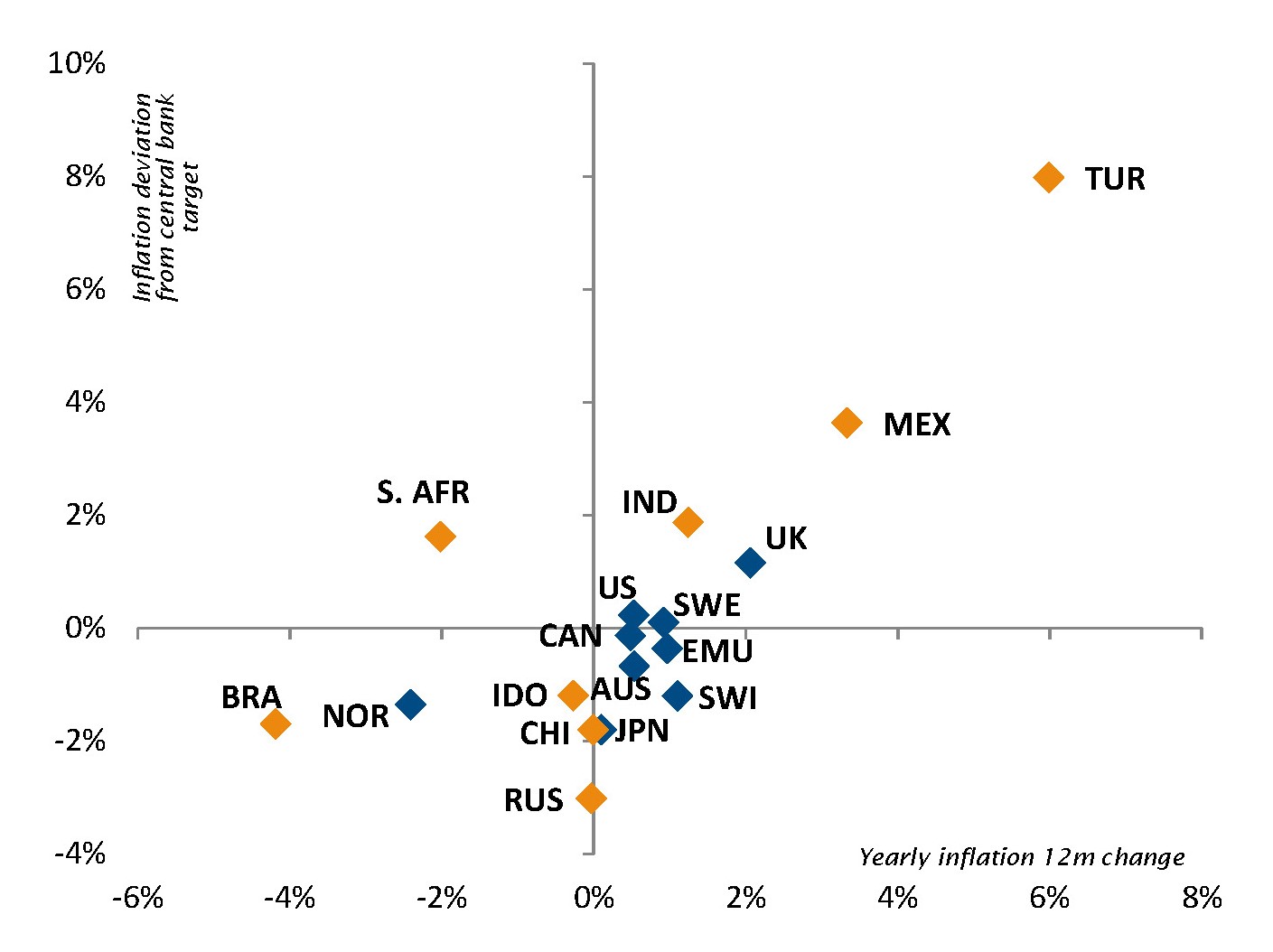

In the meantime, US inflation continues to surprise on the downside despite low unemployment, higher commodity prices and strong growth. It is the same story for the other major developed economies: inflation, or rather the lack of it, is allowing central bankers to err on the dovish side. On top of the usual structural factors such as ageing, low productivity and debt overhang, the Amazon effect seems to have also kept inflation at bay as, thanks to technology, supply now tends to adjust as fast as demand. Looking forward, we now see upside risks to growth in the first part of 2018, especially in the US, while inflation is also expected to show more clear-cut signs of bottoming out around the end of the first quarter.

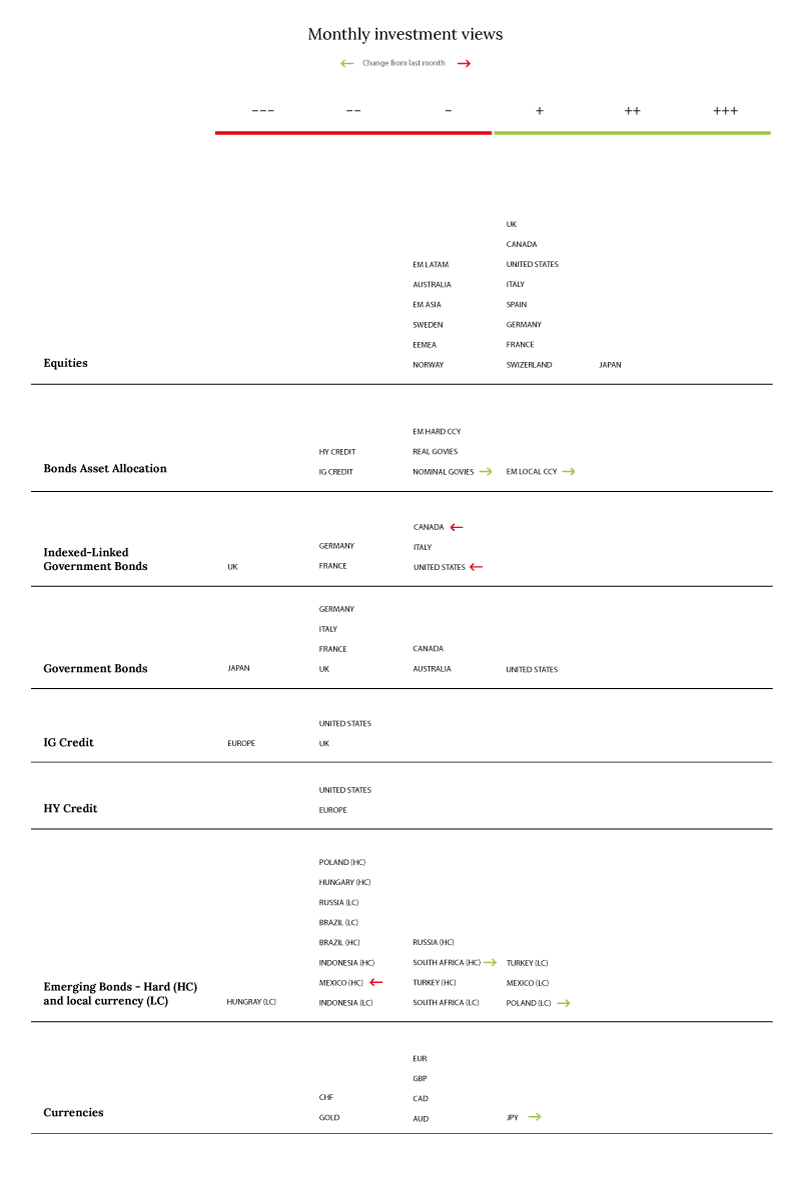

We are keeping a constructive stance on risk in our portfolios, favouring equities (especially Japan, then Europe and finally US), over credit. The overall high yield segment offers little upside potential, except a meagre carry - that is even lower than the dividend yield on the European markets - while being at risk from fading economic momentum and/or higher inflation and so rates normalisation at some point next year. A greater scrutiny and selectivity is thus warranted. A few specific names, such as Mexico and Turkey, in EM hard currency and local debt continue to offer some relative yet unexciting value.

Even if we don’t believe in a surge in inflation and a massive bond sell-off (we instead foresee a "timid" bond bear market), our duration stance was kept at a disinclination. In the current economic context and risk-on financial environment, the path of least resistance for rates remains on the upside. The least bad choice is US duration and preferably through inflation-linked instruments. As usual, our main concern remains a sharp repricing of the long end of the government bonds curves that could translate into downward adjustments for valuations across many asset classes. Inflation is the ultimate enemy of financial assets. However, equities should not adjust abruptly as long as inflationary pressures are benign and the final level, the speed of rates increases, and the underlying reasons remain reasonable (i.e. are in synch with the macro backdrop). To sum up: good times should keep rolling as we enter into the New Year.

_Fabrizio Quirighetti