We have been turning to TINA (there is no alternative) to explain the equity markets rally over the last few years, but it seems that we have now moved to FOMO (fear of missing out) to explain the the way the year started with a bang for equity markets. On one side, investors are getting more and more confident, or at least reassured by the current solid and synchronised momentum in global economic growth that was a missing ingredient since the Great Recession. On the other side, central bankers are still waiting for more inflation pressures before starting to remove the massive accommodation they put in place after the crisis. It is no wonder, then, that assets valuations are getting stretched. So far, so good and we can’t rule out that last year’s rational exuberance could transform this year into a more irrational form - next step, euphoria? It will obviously depend much on inflation trends and monetary policy. As we don’t expect significant changes in the next few weeks, the party should continue for a while and thus we haven’t changed our positioning. We have kept a constructive but contained and selective stance on risk, especially on Japanese and European equities, as we are still waiting for a dollar rebound to unlock the relative attractiveness of their valuations compared to US markets. We prefer equities over credit and some EM local debt over overall EM equities. No change either on the duration side (disinclination), where the path of least resistance for rates still remains on an uptrend. Looking forward, we believe some (contained) prices pressures should start to appear by the spring. Inflation rates will then normalise gradually to around 2-3% in developed economies (but no more than that). At the same time, on March 21st, Jerome Powell will lead his first FOMC meeting. Expectations on Fed fund rates will be revised higher thanks to a more hawkish tone, in synch with upward revisions on growth and inflation forecasts. The pressure and attention will then move to the ECB, which, at some point, will clarify its intentions and timeline about the end of QE and first rate hike. Finally, BoJ, SNB and other major central banks in developed economies will get their heads out of the woods. As long as investors adjust, or rather anticipate, gradually to this new environment, which will become less favourable at the margin, there shouldn’t be severe damages. Just expect volatility to pick up and a less clear-cut upward trend on risky asset prices. The risk during this goldilocks tapering moment is in balancing the different forces, such as rising interest rates, monetary policy normalisation, economic growth and inflation expectations, that are playing together and will deform valuations. Unfortunately, as we already experienced several times in the past, elastic properties of asset valuations aren’t infinite: if you pull them too far or too fast, they will come back, or even break, at some point.

_Fabrizio Quirighetti

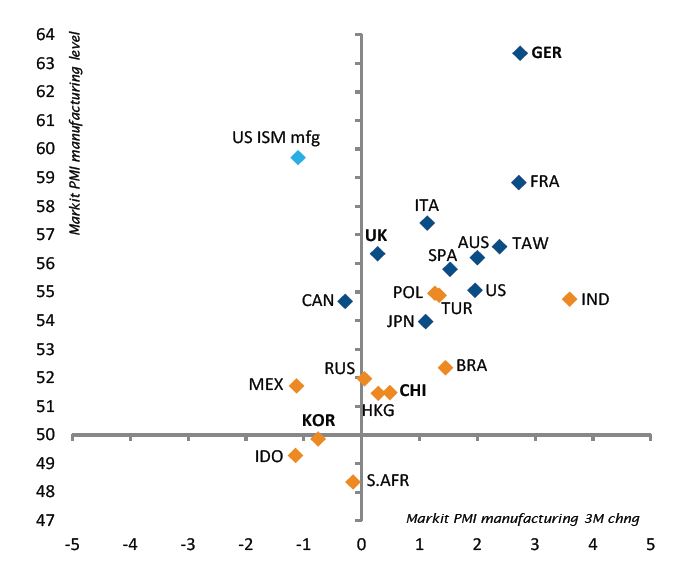

- Economic expansion and momentum remain firmly positive among advanced economies.

- Rate markets may start to anticipate less supportive monetary policies going forward, leading to less accommodative financing conditions.

- The relative preference of equity markets versus bonds remained unchanged over the period.

Testing the elastic

Economic backdrop in a nutshell and global economic review

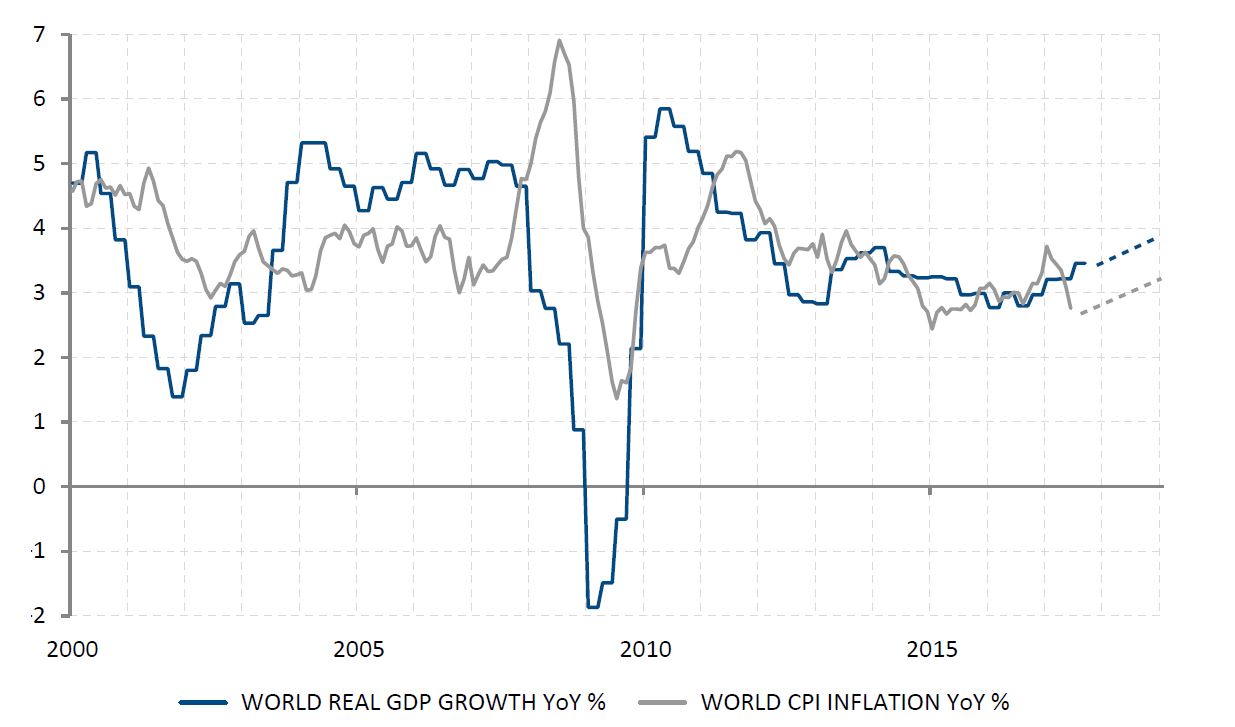

“The Current Economic Sweet Spot Is Not the New Normal” warned the IMF in January. However, investors could be forgiven for thinking that this is some kind of customary disclaimer. Indeed, the Fund’s projections are positive, raised to 3.9% for global growth in the next two years on the back of higher expected US and European GDP expansion. And monthly economic indicators continue to surprise on the upside across advanced economies. As a result, commodity and energy prices are picking up, lifting growth further in producing countries.

This is precisely why the IMF warning is probably very timely: this “Current Economic Sweet Spot” has resulted from strong growth now being, so far, matched by consumer price inflation, allowing economies to have their cake and eat it - i.e. maintain very accommodative monetary policies and enjoy the best global growth in half a decade at the same time. Such a sweet spot is unfortunately unlikely to last for long, as the business cycle dynamic finally translates into an uptick in inflation rates, with rising commodity and energy prices reinforcing the trend. No misunderstanding here: these are NOT negative developments, rather “normal” ones to be welcomed as indications of a growing global economy. But they could trigger yet another “normal” development: rate-sensitive markets may anticipate less supportive monetary policies going forward, leading to less accommodative financing conditions. If this happens in the coming months as we expect, and soon after a repricing of rate markets, the global economy will leave behind its current sweet spot for a more normal environment. Factors such as weak demographic and productivity trends will though have a dampening impact on potential growth rates and hyper-interest rate growth sensitivity will keep growth and inflation momentum in check.

Growth

Economic expansion and momentum remain firmly positive among advanced economies, with improving dynamics in some, especially oil producing economies. The growth picture is less spectacular in emerging economies but is nonetheless positive across the board.

Inflation

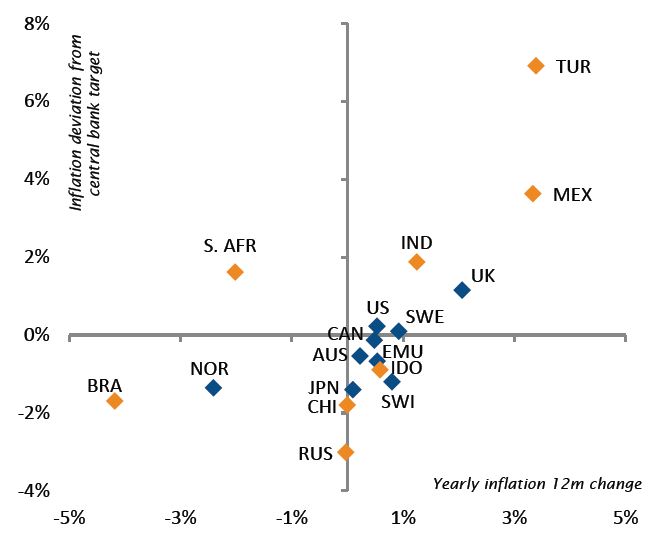

The key macro indicator remains subdued among most advanced economies for the moment but is expected to pickup in the coming months. Emerging economies exhibit more heterogeneous dynamics.

Monetary policy stance

In a nutshell, still very accommodative in advanced economies, but with a trend toward some normalisation, while mostly restrictive (to different degrees) among emerging economies without a clear trend.

Such a sweet spot is unfortunately unlikely to last for long as the business cycle dynamic finally translates into an uptick in inflation rates.

Developed economies

All recent economic data have confirmed the strong growth momentum in the US economy at the turn of the year, with the vote for tax reform even providing additional support to sentiment (before possibly marginally spurring business and consumer spending). As such, after likely recording a third consecutive quarter of above-3% growth in Q4, the US economy enters 2018 on a strong footing, with short-term risks tilted to the upside both in terms of activity and inflation. In this context, once at the Federal Reserve from early February, new chair Jerome Powell will have a relatively easy environment to contend with; he has many reasons to continue to raise US short-term rates, and so far no incentive to change the gradual pace of the rises.

The situation is paradoxically slightly more complicated to handle for Mario Draghi on the other side of the Atlantic, although the European Central Bank (ECB) undoubtedly prefers its current challenges than the potential of Eurozone breakup risk, monetary policy fragmentation, failing transmission of policy via the banking channel, bank undercapitalisation or the deflation risks, all of which the institution has had to handle in the past decade. Still, the strong improvement in growth conditions across the Euro area, even with inflation rates still below the ECB target, raises the pressure on the central bank to at least communicate its post-QE outlook and the timing of future rate hikes. Future markets are already repricing a faster-than-expected path for EUR short-term increases, pushing the EUR up on FX markets. The trick for Mario Draghi is to manage the speed of this welcome normalization, in order to avoid unwelcome adverse spillovers caused by a rapid appreciation of the currency and a tightening in financial conditions.

This dilemma is faced by virtually all central banks of advanced economies that haven’t started the normalisation process yet (Nordics, Japan, Australia, Switzerland): removing some of their extraordinary monetary policy support as it is increasingly less needed, without endangering the ongoing positive growth dynamic. This will be the key macro debate of 2018.

Emerging economies

External factors continue to support the growth dynamic in most emerging economies. Strong demand coming from advanced economies are fuelling export growth in Eastern Asia and in Europe. Rising oil and commodity prices support economic expansion in producing countries such as Russia or Brazil. On the other hand, this increase in oil prices may be threatening oil-importing countries with a current account deficit such as India, Turkey and South Africa.

However, positive EM FX trends in 2017, with the appreciation of most EM currencies against the USD after the decline of the previous years, helped to contain inflation, with the exception of Turkey, Mexico and South Africa, which are faced with idiosyncratic endogenous upward price pressure. This allows East Asian and Eastern European central banks to run mildly accommodative monetary policies, while China aims at targeted measures to contain excessive credit growth in some sectors of the economy and the financial system.

_Adrien Pichoud

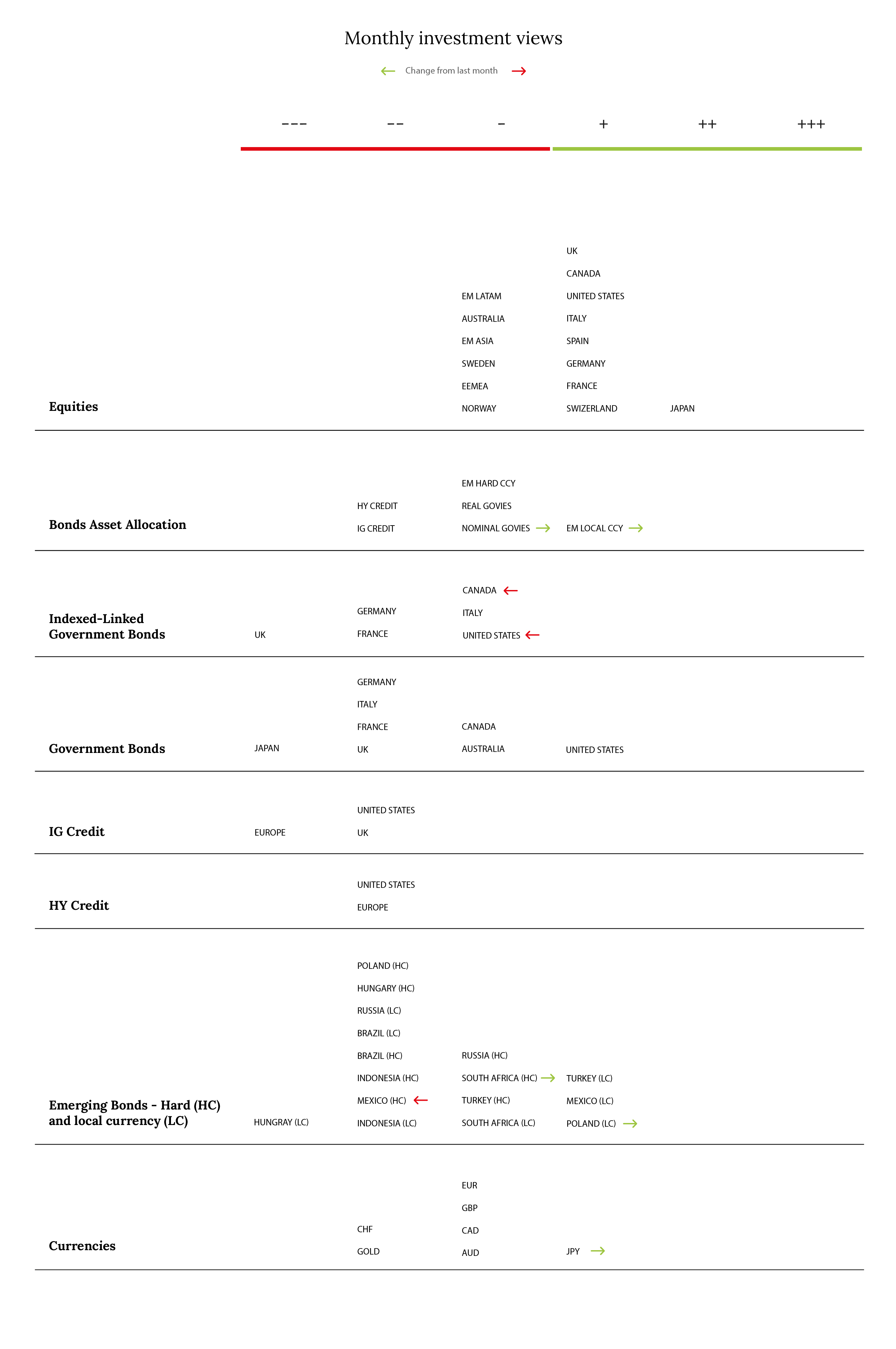

Investment Strategy Group Takeaways and asset valuation

Risk and Duration

No change in assessment

Equity Markets

The relative preferences across equity markets have also remained unchanged, with Japan being the most favoured region. This is followed by Europe, the United States and the United Kingdom, with Emerging Markets and other smaller markets in a mild dislike.

Bond Markets

While the overall preference for duration remains in a mild dislike, there have been some changes in the current fixed income asset allocation. The recent sell off in government bond markets has started to bring value back into this segment of the market; as a consequence, the segment was upgraded by one notch to a mild preference. US and Canadian linkers look somewhat less attractive at the margin and there have been some small changes in the assessment of single emerging bond markets. Within developed market government bonds, US treasuries remain our top pick.

Our Risk stance and relative preferences across equity markets have remain unchanged.

As of the end of January 2018, 10-year US Treasuries were yielding 2.7% - a 0.74% increase from early September 2017. The reasons for this stark shift in treasury yields over the past few months were, on one hand, market expectations of renewed interest rate hikes by the Federal Reserve and, on the other, fears that US tax reform would intensify inflationary pressures and raise questions about US debt dynamics. Many market commentators have drawn parallels between this recent shift in bond yields and the taper tantrum. However, dissecting the drivers of both yield moves, it becomes evident that these sell-offs are very different in their nature. During the two immediate months of the taper tantrum, bond yields rose by approximately 1% - this was driven by the term premium, which is a risk premium that compensates for uncertainties with regards to monetary policy. It was also driven by the real yield, i.e. growth expectations. The risk premium for unexpected changes in inflation, the breakeven inflation, actually compressed during that time. The latest rise in yields on the other hand was driven equally by the real yield (growth) and breakeven inflation (inflation), with very little change in the term premium. While inflation is rising mildly, we don’t believe that the US or the world economy is anywhere close to an inflation scare. Moreover, some of the inflation currently haunting the market might well turn out to be transitory. This means that sooner or later, as yields (risk premia) rise, the case for buying treasuries becomes increasingly compelling. In relative terms they are clearly more attractive than other high quality bond markets.

The reasons for the stark shift in treasury yields over the past few months were, on one hand, market expectations of renewed interest rate hikes by the Federal Reserve and, on the other, fears that the US tax reform would intensify inflationary pressures and raise questions about US debt dynamics.

Forex, Alternatives & Cash

The Yen has been upgraded to a mild preference from a mild dislike. The reasons for this are as follows: the currency is cheap and the central bank is still the least hawkish of all the major central banks. So, there is still some catch up to do in terms of the Bank of Japan’s reaction to stronger growth and somewhat stronger inflationary pressures. Moreover, from a portfolio construction point of view, the yen is once again a very good diversifier and also a beneficiary of a weaker USD, which remains our base case scenario for the coming year.

_Hartwig Kos

Disclaimer

This marketing document has been issued by Bank Syz Ltd. It is not intended for distribution to, publication, provision or use by individuals or legal entities that are citizens of or reside in a state, country or jurisdiction in which applicable laws and regulations prohibit its distribution, publication, provision or use. It is not directed to any person or entity to whom it would be illegal to send such marketing material. This document is intended for informational purposes only and should not be construed as an offer, solicitation or recommendation for the subscription, purchase, sale or safekeeping of any security or financial instrument or for the engagement in any other transaction, as the provision of any investment advice or service, or as a contractual document. Nothing in this document constitutes an investment, legal, tax or accounting advice or a representation that any investment or strategy is suitable or appropriate for an investor's particular and individual circumstances, nor does it constitute a personalized investment advice for any investor. This document reflects the information, opinions and comments of Bank Syz Ltd. as of the date of its publication, which are subject to change without notice. The opinions and comments of the authors in this document reflect their current views and may not coincide with those of other Syz Group entities or third parties, which may have reached different conclusions. The market valuations, terms and calculations contained herein are estimates only. The information provided comes from sources deemed reliable, but Bank Syz Ltd. does not guarantee its completeness, accuracy, reliability and actuality. Past performance gives no indication of nor guarantees current or future results. Bank Syz Ltd. accepts no liability for any loss arising from the use of this document. (6)