We expect the dollar to weaken in the second half of the year, with a target of 1.30 against the EUR at the end of 2018. Here are the reasons that support that view:

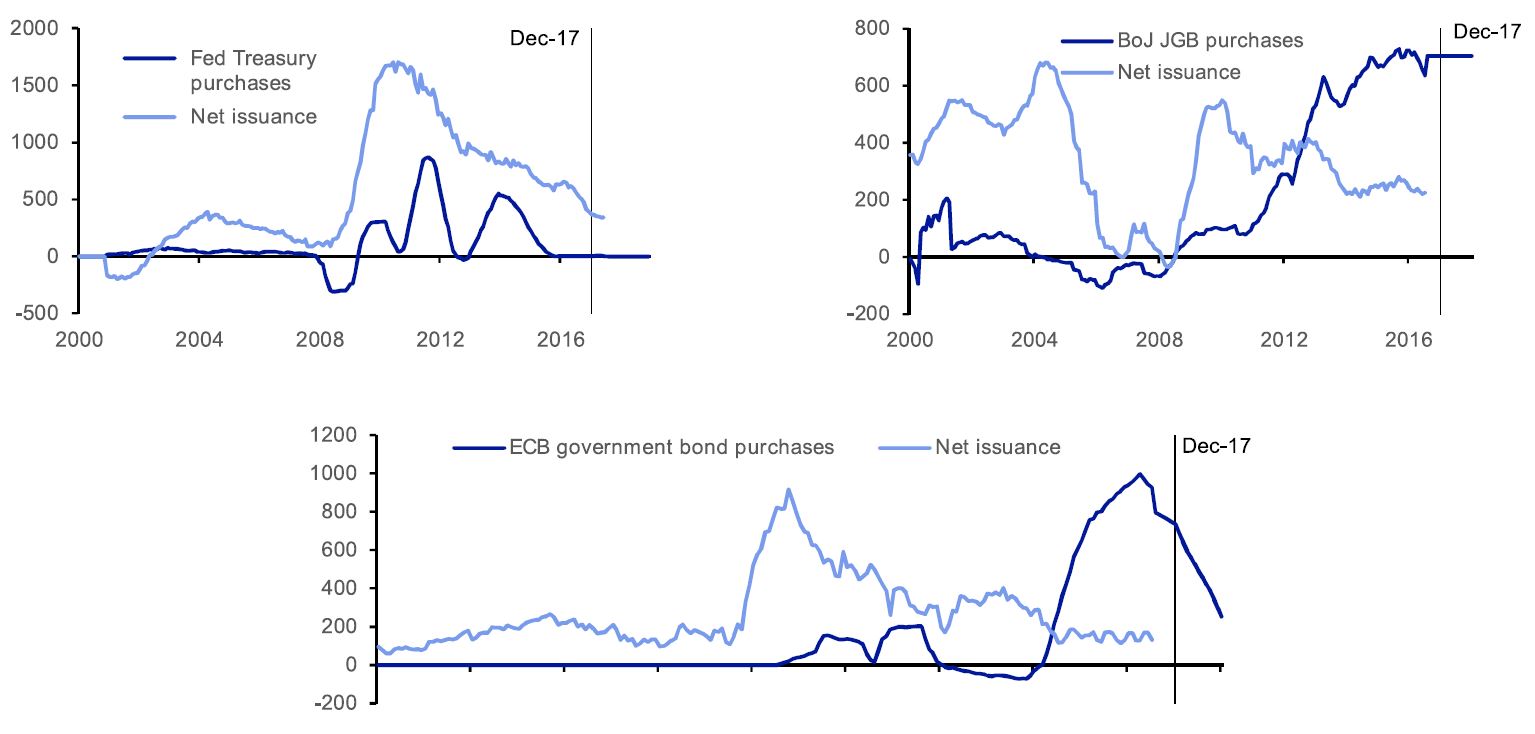

The Federal reserve’s (Fed) path to tighter financial conditions is now largely priced-in by the markets, while on the contrary, normalization of policy from the European Central Bank (ECB), Bank of England (BoE) and Bank of Japan (BoJ) has not or has hardly begun (the ECB and the BoJ are still keeping up with the Quantitative Easing!).

The transition to a cycle of gradual interest rate increases from other major central banks will be key for the foreign exchange market which will, in relative terms, make the greenback less attractive.

In a context where the European and Japanese economies are also less advanced in their expansion cycle than the US economy, and where the Euro Zone and Japan have current account surpluses of around 3% of their GDP, economic fundamentals point to a phase of strengthening of the Euro and, after, of the Yen, against the dollar and the American "twin deficits" (external and budgetary).