There is a sea of change on financial markets compared to one year ago, as we moved from excess pessimism to some form of irrational hope. Sentiment is clearly supported by a more favourable economic backdrop : activity indicators are globally picking up, inflation is moving higher and major developed central banks are either finally contemplating to hike or, at least, not hinting to cut rates further into negative territory. However, it’s worth noting that firstly, rates are already at very low levels in terms of economic growth, inflation and key policy target rates, and secondly, we don’t expect meaningful or sustainable overshooting in these three key variables in the future as the nasty trinity of poor productivity gains, muted labour force growth and high indebtedness remains in place. In other words, our medium-to-long term scenario hasn’t changed, growth will continue to come through, core inflation will tend to undershoot central banks’ targets and thus monetary policy will err on the accommodative side.

While last year there were plenty of reasons for investors to get concerned and scared enough to sell equity at their bottom levels, which we avoided, we are now struggling to find a consistent narrative to be overly cautious and drastically reduce our risk stance. We are sceptically optimistic. It’s quite difficult to predict what could go wrong in the next few weeks in order to derail the current tailwinds : European political risk premium has shrunk, Chinese woes have been removed on the border line, rates aren’t high enough to weigh on the overall equity markets, central banks won’t deliver a nasty surprise and economic momentum should remain strong. As complacency is now king, we are in fact concerned by stretched valuations on both equity and credit markets. The margins to absorb any negative, unknown surprises are thin as they are already pricing the perfections described here above.

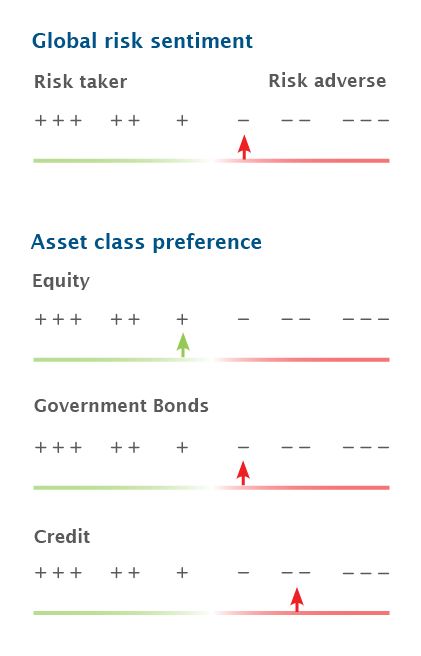

Consequently, we are taking some chips off the table by reducing our overall risk stance from mild preference to mild disinclination. We are keeping some reflation trades on the equity side where there is still some upside for valuation and economic backdrop reasons, even if the outperformance may not be as clear going forward as it has been over the last few months. Selected EM debt exposure - with Mexico and Turkey being our top picks - and some duration exposure through US treasuries are starting to offer some value both in terms of valuation and portfolio construction. After buying on the sound of cannons, we now opt to reduce on the sound of the Trumpets.