Equity markets have had a flying start to the year so far, contrasting with the doom and gloom of last December. The key question is thus: "Is it a bear market rally or a new bull market?" We tend to favour the first proposition. Obviously, there was some dislocation, exaggeration and a few bargains for the bravest at the end of 2018, but what has really changed over the last few weeks in order to turn us more bullish – especially after the recent quick rebound?

On the macro side, the economic growth backdrop has continued to deteriorate. This can be seen in Europe and Japan, which are now flirting with stagnation, but also in the US, as the fiscal stimulus boost gradually fades away – the government shutdown won’t help Q1 figures either. There have been some tentative signs of stabilisation in Chinese data, vague announcements of additional easing policies, and recent hope about a trade deal with the US, which may turn out to be just a truce. As a result, don’t expect any stabilisation in growth before spring… at best.

On the inflation front: it remains muted and well under control, even after ten years of expansion in the US and major developed market (DM) economies. Bond and inflation vigilantes, who finally had a few hours of glory last year, suddenly disappeared in Q4 with the meltdown of oil and risky assets.

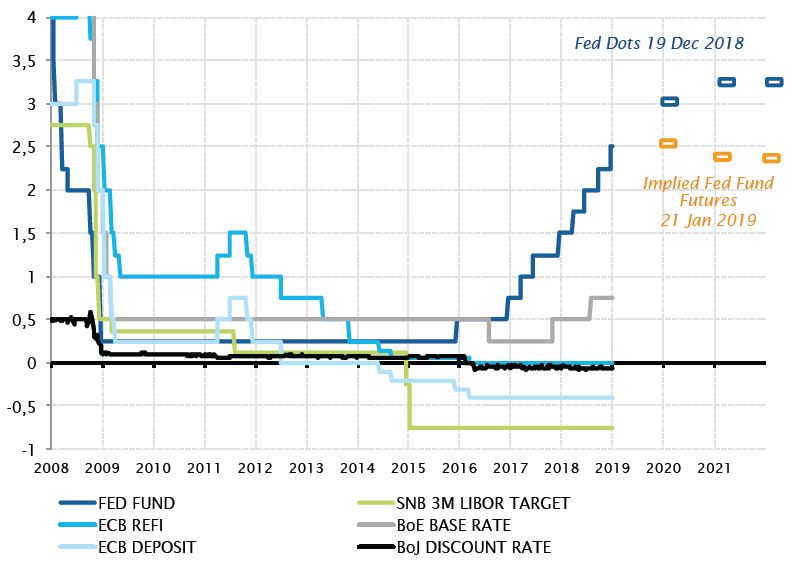

As a result, the only significant change has been the Fed’s rhetoric. What Jerome Powell had broken in October by appearing too hawkish, he has now repaired by massaging investor sentiment with words such as ‘patient’, ‘flexible’ and ‘data dependant’. The Fed came back just in time to stop the bleeding before it got out of control. So, what now?

There are two potential scenarios. Either growth picks-up in the second half of this year, and the Fed will have to continue to normalise – as well as other DM central banks – pushing down the valuations of assets which may not have had enough appeal when compared to a positive real return on plain vanilla cash. Or growth dies slowly in a long, soft landing – we don’t believe in a nasty and sharp recession scenario at this point – and dream on an upside surprise on earnings for the next few quarters.

In conclusion, equities should remain range bound, and rates capped for the next few months. Thus, we remain cautiously constructive, being somewhat underweight on both equities and duration, especially on the euro curve, with some dry powder to redeploy when valuations become more attractive. As the debt clock continues to tick and DM central banks are running short of effective ammo, an allocation to gold makes sense today. A zero yield is actually better than the promise of negative yield on about $8trn of indebted government bonds.