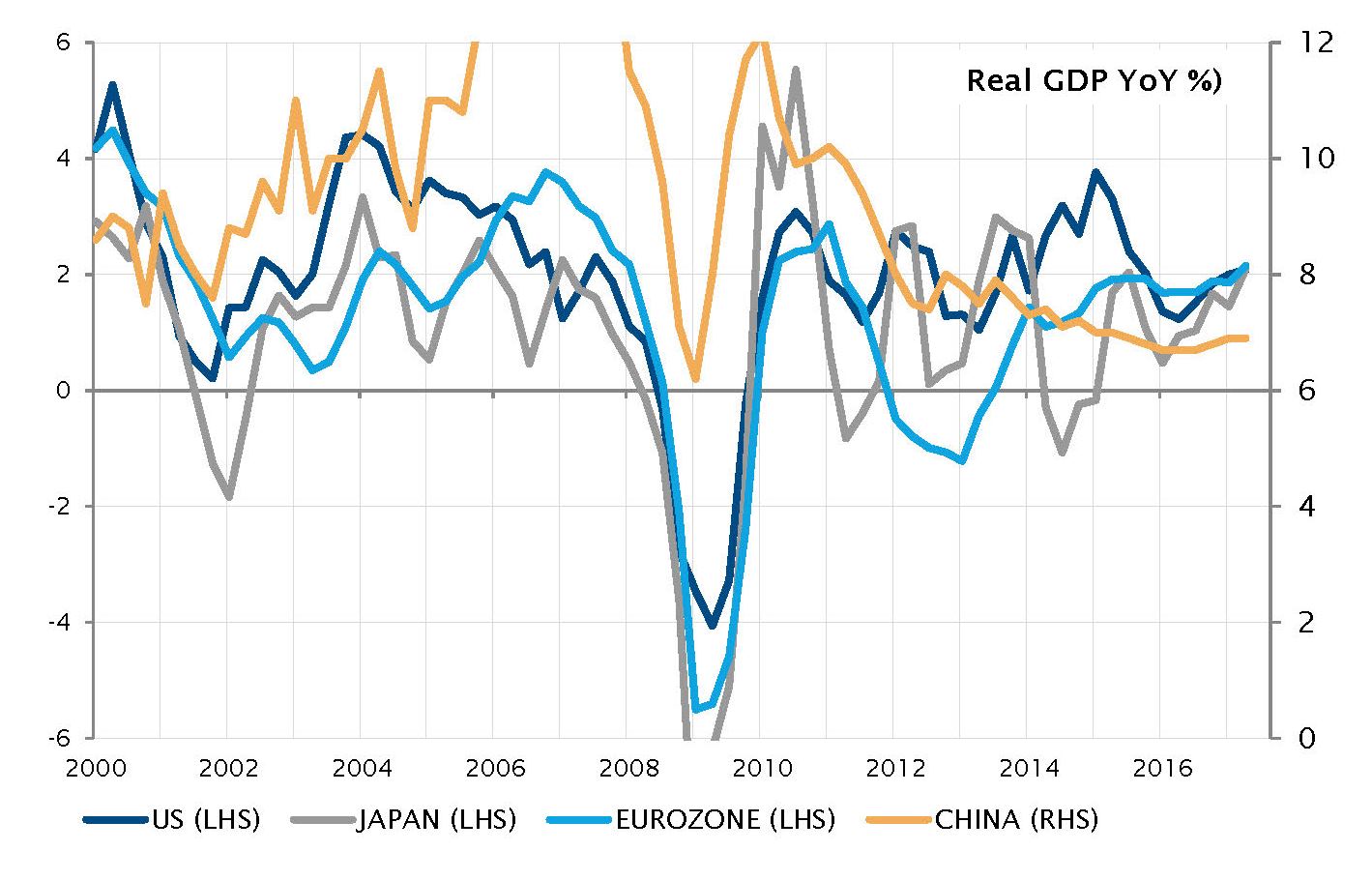

Let’s get straight to the point: there haven’t been any material changes in the economic environment, our asset valuation analysis or in our risk framework to recommend significant changes in our positioning. Not even Trump’s tweets or some geopolitical challenges, such as tensions with North Korea, the Venezuela crisis or new terrorist attacks in Europe, seem able to alter the current = economic backdrop of global synchronised growth with low inflation and very loose monetary policies.

In the meantime, the earnings season has also been supportive, especially in the US with high positive earnings and a top-line sales beat ratio of around 70%. It was more mixed in Europe as expectations were probably too high. Nevertheless, sales and earnings growth of respectively about 7-8% and 15-16% year-on-year can’t be seen as bad. The rapid appreciation of the euro over the summer (helped to some extent by the dollar’s weakness) has weighed on the European equity market’s performance in local currency. With a more stable euro-dollar relationship going forward and even a likely pullback towards 1.15 in the next few months, the potential for outperformance in European equity remains intact for valuation purposes. We have tactically downgraded the euro to a mild disinclination stance (against USD) and reiterated our preference for European equities.

Is inflation late or dead? It seems to be the $100m question for both central bankers and investors as there is now a clear consensus surrounding economic growth. While the current synchronised expansion is far from spectacular, it offers other advantages as it is a global and very steady phenomenon, meaning low volatility and contained uncertainties. So, the process of normalisation now essentially relies on the inflationary cycle. In this context, Jackson Hole has been a non-event that could be summed up as: "looser for longer but please don’t remove banks’ regulations". It reminds me of a swarm of fireflies asking firemen to remain cautious and close enough to prevent a disaster. Central bankers and some investors think inflation in goods and services is just late, but we believe it is dead. Current monetary policies are now much more effective at creating asset price inflation, distortions in the financial system and rising imbalances, which need still more regulations and firemen to control them.

Looking forward into September, we don’t expect meaningful changes to central banks’ exit strategies to arise from the next European Central Bank or Federal Reserve meetings. However, the US debt ceiling debates are looming and may lead to some volatility spikes by the end of September. US politics, and the Trump administration in particular, are much more volatile and unpredictable than economic growth, inflation or central banks decisions. We just hope their decisions won’t have a lasting negative impact.

_Fabrizio Quirighetti