Godot finally arrived. After nine years and three quantitative-easing programmes (QE 1, 2 and 3), the Fed began to reduce its balance sheet this month. As the ECB prepares to begin tapering, the Americans have already entered the era of unwinding and monetary-policy normalization. The US isn't just strong, they're always ahead of the game...

...and their actions here are not crazy in the least! They are taking care not to frighten the markets, which have been among the great beneficiaries of the extremely loose policy. If, like Janet Yellen and most of the central bankers, you are bemused by the "mysterious" disappearance of inflation in prices for goods and services, you will at least agree that monetary policy has had the expected effects on inflation in prices for financial and real-estate assets. The Fed will therefore move slowly: it will simply stop reinvesting some coupons and bonds that will expire. It will also initially limit this automatic but highly controlled unwinding to $10 billion a month, and then gradually raise the limit to $50 billion. I'll spare you the calculations: less than $300 billion in 2018, and no more than $600 billion the following year. In short, Ms Yellen says it will be "like watching paint dry."

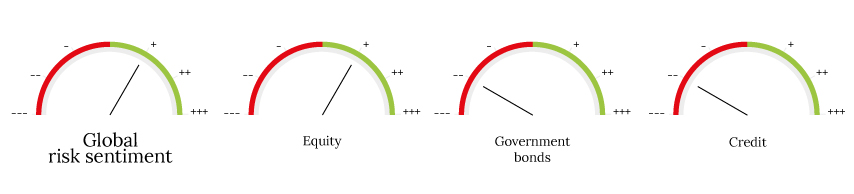

But markets and investors—us included—are anxious. Hence a certain apprehension regarding US long-term interest rates (if they rise too quickly) and the credit market (if liquidity evaporates). It's sort of like the wave of uneasiness you get as the airplane takes off and you briefly consider the possibility of an unlikely but potentially disastrous accident. But let's try a bit of positive autosuggestion, so that we don't give way to an unfounded panic. Although the Fed and the US are at the heart of finance and the global economy, other major central banks, such as the ECB and the BoJ, will continue to experience swelling balance sheets. The net sum of the major central banks' balance sheets will therefore increase further next year. Plus, with interest rates still near zero in most of these economies, it is unlikely that US long rates will soar on their own. Finally, the market's reaction to the Fed's reduction in its balance sheet—or its monetary tightening via rate hikes, the next of which may come as early as December—will also depend on the economic context in which they arise. I can’t imagine US Treasuries selling off solely because of monetary tightening if nominal growth suddenly nosedived...

Economic expansions and bull-market phases have never died from old age, so it's still (much?) too early to worry. And I'm not just saying that for self-reassurance!

_Fabrizio Quirighetti