After their failure to fulfil a pledge to reform the US health care system, the Republican legislators are determined to enact some type of tax reform before the end of 2017. Currently, the House of Representatives has passed its version of the bill and the Senate version is through the Finance Committee and is expected to be put to a vote of the entire Senate before the end of November. The two versions are similar, but do have some differences. If the Senate passes their current bill, the House and Senate will enter the reconciliation process. There is a possibility that the two sides will not be able to agree on a final bill and that reconciliation will fail. In that case, they will need to begin again, most likely in 2018. In the meantime, we are focusing on the possible impacts of the current versions of the two bills.

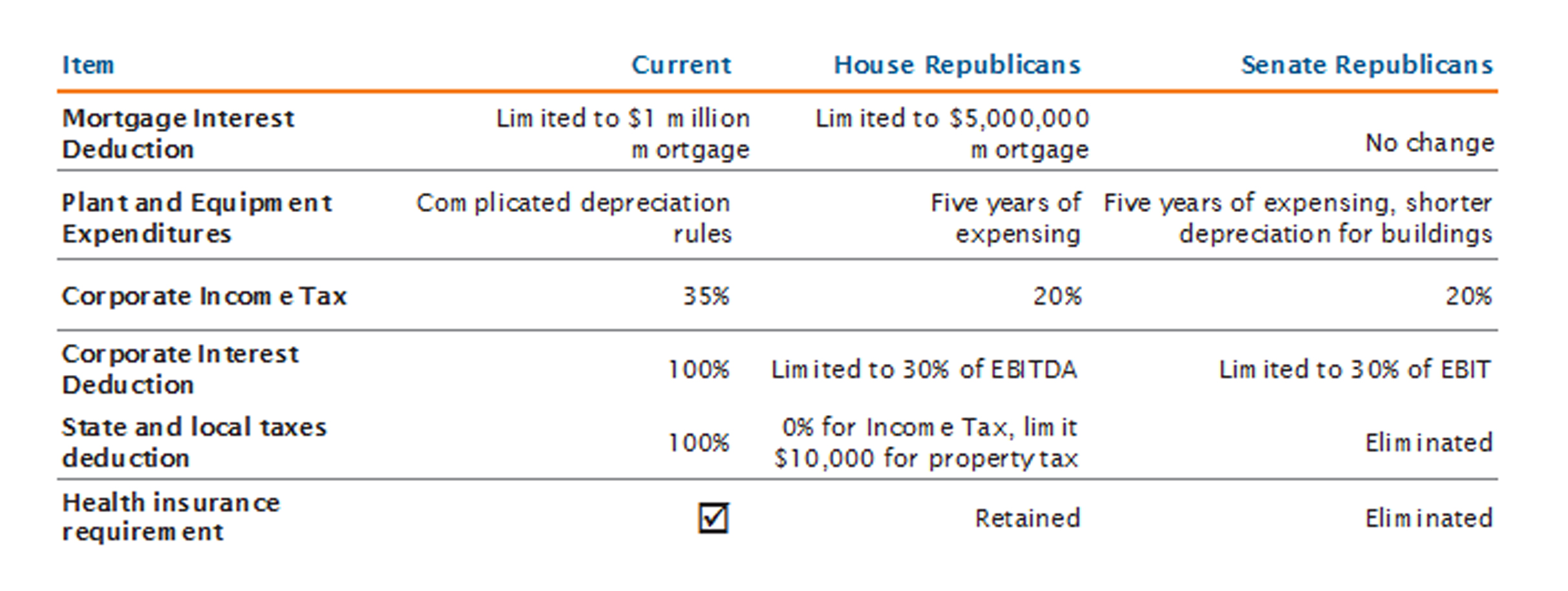

The main focus of both bills is to reduce the Corporate Tax rate from 35% to 20%. The US rate is now an outlier globally as other countries have lowered their rates to make their domiciles more competitive. There is no consensus about how this will affect the economy. The reduced taxes could be used to boost capital expenditures, increase wages and/or add jobs, pay out dividends or buy back stock. The theory is that the economy would benefit from a boost in productivity from increased capital expenditures. Or, consumption would rise if the tax cut is passed on in the form of higher wages or improved employment which would result in growth in consumption. If the cut is used to pay dividends or buy back stock, the overall economy might not benefit, but the equity markets would. We remain hopeful that the proposed changes, if enacted, will benefit the economy.

Since we manage high yield portfolios, our focus has been on the possible effects on companies rated below investment grade. A few specific measures of the bills would have direct effect on high yield issuers. Both bills propose a limitation on the deductibility of interest expense with the Senate bill being the stricter of the two. We have analysed the expected impact on companies and concluded that the limitation would be a burden to certain highly levered issuers with weak cash flow. However, the majority of issuers would not hit the threshold. This limitation would change the economics of leveraged buyouts and could discourage the use of large amounts of debt to take companies private.

Some of the provisions would benefit or harm specific sectors. The possible expensing of capital expenditures would be positive for certain industries including those involved in large infrastructure projects. On first look, the elimination of the exemption of state and local taxes as well as limitation on the mortgage interest deduction might disadvantage home-builders. However, when examined more closely, most home-builders operate in low tax states and build less expensive homes that would not carry mortgages larger than the maximum deduction. With the difference in tax rates narrowing and the proposal of additional taxes targeting offshore intellectual property, inversions where companies establish headquarters outside the US would become less attractive. The Senate bill also includes a controversial provision to remove the requirement that individuals purchase health insurance, which could lead to further instability in insurance markets. Hospitals and other healthcare service providers benefited from the decrease in uninsured patients when the mandate was put in place. A portion of this advantage could reverse if the requirement is eliminated.

Overall, we believe that the bill would be positive for balance sheets because reducing the tax rate would raise the after tax cost of capital which increases the incentives for companies to pay down debt. This could be a positive for the high yield market as issuers delever and strengthen their balance sheets. It is less obvious what the effect would be on the overall economy and, as a consequence, the impact on corporate revenues. It all depends on where the increased after tax income is spent. Opponents of the bill claim that it will be used to aid shareholders. Advocates believe that the tax cut will flow to higher employment, wages and investment.