Historically, risk premia have been exploited by hedge-funds and proprietary trading desks at banks as alternative sources of returns from equities and bonds. It is only since the end of the Financial Crisis that liquid, transparent and cost-efficient products aimed at delivering risk premia returns to investors have been developed. According to Citi Research, the assets invested in risk premia strategies are expected to grow to $2.1 trillion by year-end, from $265 billion in 2015.

Premia-based strategies provide a cost-efficient alternative to equities and bonds and hence could find a place in every portfolio. However, because they are different from traditional asset classes, many investors wonder how to use premia in their overall asset allocation and what key roles the strategy can play. Investors may question whether it is a good time to invest in premia in an environment that is characterized by low inflation and low interest rates as well as by very expensive equity markets? A reasonable investor will ask themselves how will premia fare and what impact could it have on an overall portfolio risk/return profile when, for example, the stimulus programs implemented by central banks are brought to an end?

Blending premia can be particularly interesting as different premia tend to perform in different macro-economic environments. Portfolios that combine a number of premia can expected to perform throughout market cycles and offer a welcome diversification from both equities and bond. This is particularly important in a time when mainly equity and bond valuations are stretched with investors rightly seeking ways to preserve capital and generate stable return while reducing their overall risk profile.

Finding diversified and stable source of returns in an uncertain macro-economic environment

Monday, 02/26/2018What do traditional value investors and cryptocurrency traders have in common? Very simply, they try to profit from the irrationality of other market participants. Value investors exploit cheap firms which are overlooked by investors, while cryptocurrency traders benefit from herd effects that draw market participants to keep buying in spite of exceptionally strong returns based on uncertain fundamentals. Irrationality is nothing new in financial markets. It is also well-known, and even academically documented, that patient and disciplined investors can employ strategies to exploit these inefficiencies and make a profit. This fact is at the heart of what is known today as “risk premia” investing.

“Equity premia have been immune to interest rates moves as well as to inflation surprises and all the while have delivered attractive and stable returns. Furthermore, thanks to a low correlation with equity markets, they can provide a safer alternative to equity and bonds.”

The world of equity risk premia

Though there are premia in every asset class, we will concentrate on those present in equity markets. Although they exist in the same asset class, equity premia can exhibit a range of very diverse behaviours depending on the macro-economic environment. Also, as we will see, their combination in a portfolio can bring a number of great advantages.

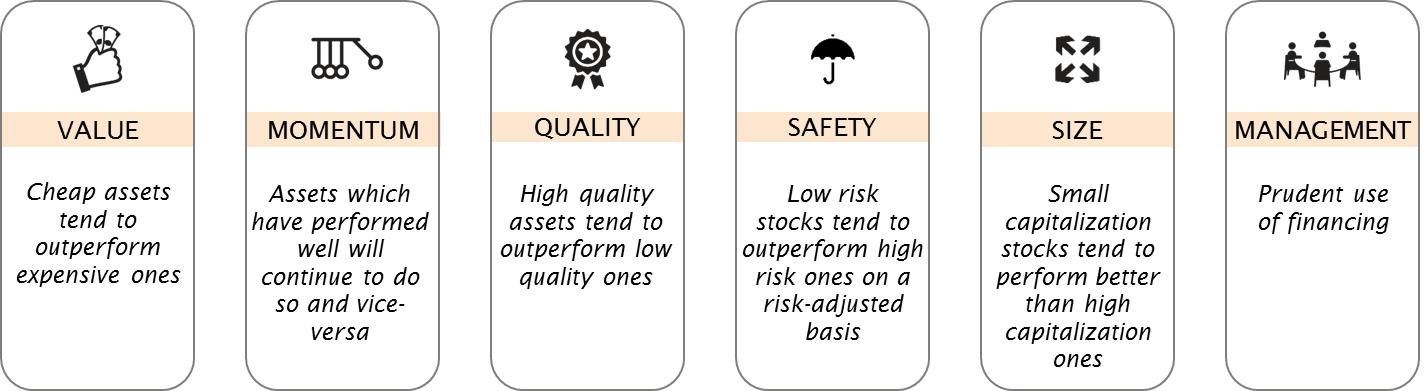

There are essentially 6 main risk premia present in equity markets (see Figure 1). ‘Harvesting’ risk premia in equity markets is done employing a long-short approach that results little net exposure to equity markets. For instance, profiting from the “size” anomaly is done by taking ‘long positions’ in small companies while selling ‘short positions’ in large companies. Both academic as well as empirical market research have shown that the profits from this strategy are significant as over time, small company stocks as a whole tend to produce better long-term returns compared to larger company stocks. However, it is important to understand that although positive returns can be expected over the long-term, there are periods when small companies may suffer more than large companies - for instance during economic recessions.

Another example is the risk premia that can be harvested by investing in firms with very stable revenues, defined as “low-risk”, which tend to outperform “riskier” businesses, especially during recessions.

What an investor may quickly realise is that by mixing ‘small company’ risk premia with ‘low risk’ risk premia, they can create a strategy that generates strong returns over time, while making their portfolio more resilient to market cycles – especially market dislocation events. Indeed, the “small-size” premia should generate returns in inflationary environments, while the “low-risk” component is meant to protect the strategy in recessions.

This is just an illustration of how two premia that perform well in different market environments can generate a more stable return profile when combined. We believe that a far better result can be obtained by moderately expanding the number of risk premia. The key idea in end however is that by blending premia, one can produce a portfolio that may have at least a couple of performance engines switched on during every market environment. It is worth noting that blending premia causes complexity, and therefore multi-premia strategies greatly benefit from the intrinsic discipline and risk management capabilities of computerised systems that are developed and managed by quantitative market experts.

Equity premia in the new normal

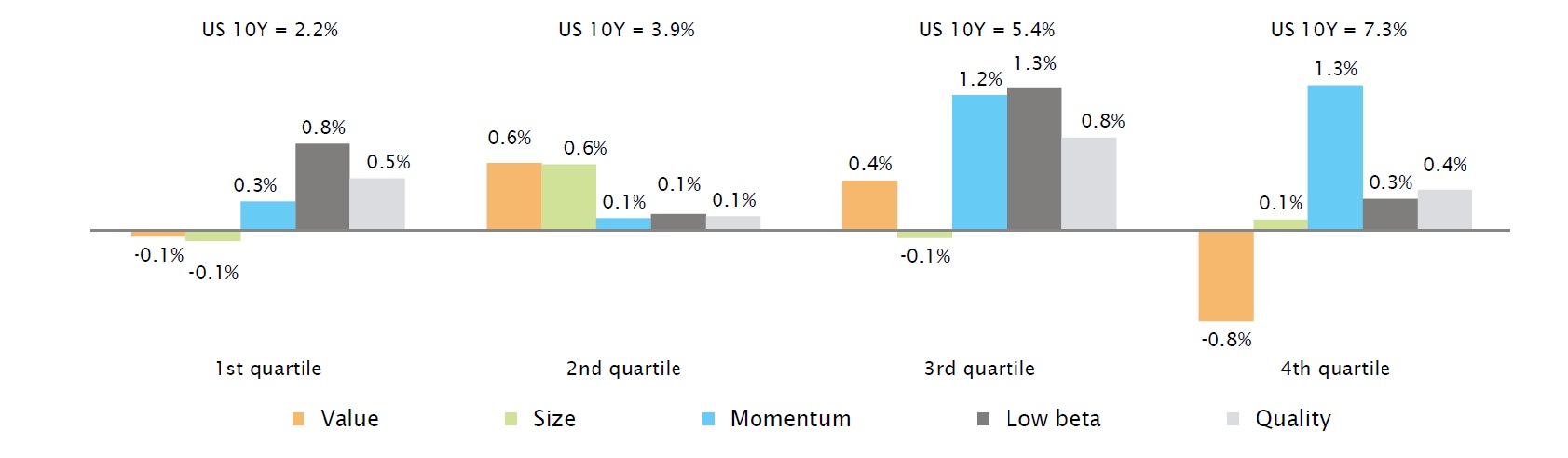

In the current context, a great advantage of equity premia is that their combination can be quite robust to interest rate hikes (or strong moves in general). Indeed, we find that most premia are not affected by interest rate levels. In Figure 2, we show that most historical performance of North American equity premia was up when the average level of the 10Y interest rate was high (far right of chart below). However, their performances were also positive on average in periods when interest rates were low (far left of chart below).

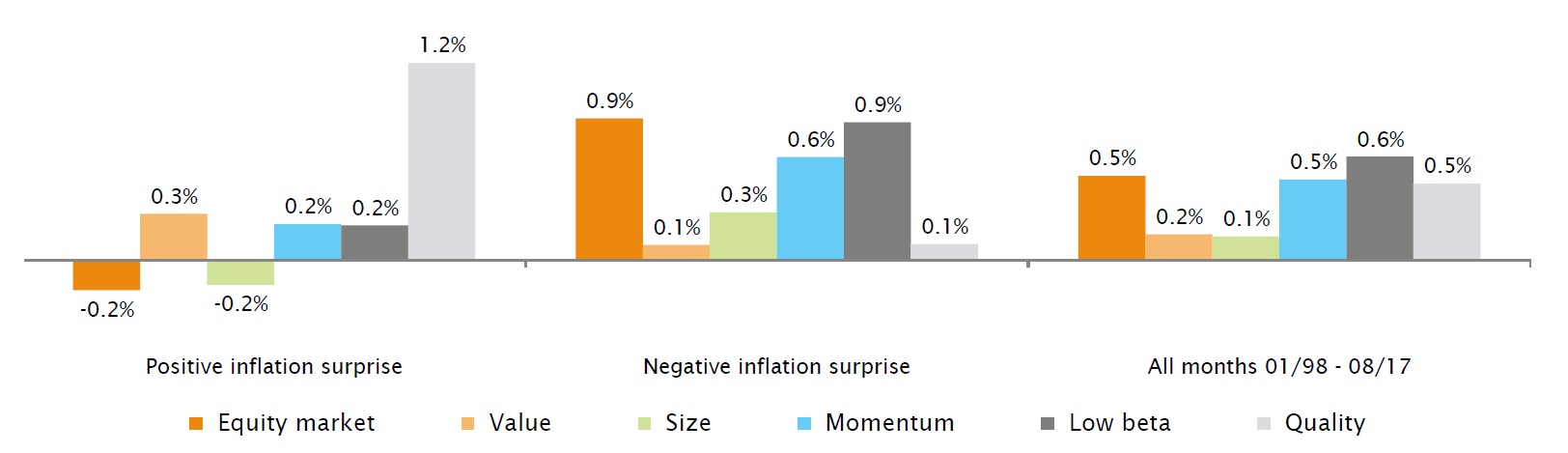

The same robustness can be observed with respect to inflation. The empirical data shows us that the effect of inflation on equity premia has not been much actually. Figure 3 shows the monthly performance of main North American equity premia when inflation surprised upside and downside as expressed by the Citi Research Inflation Surprise Index.

As we see, both equity markets and small capitalizations stocks (size premia) react negatively when inflation surprises on the upside. On the other hand, we see that all our equity premia experience a positive average monthly performance when inflation comes in below expectations. The benefits of having a blended allocation to risk premia can also be seen in this chart, as the Quality premia performs best when inflation comes in too strong, while the Low Beta premia performs best where inflation is muted.

Conclusion

In a world where finding stable, diversified sources of returns is difficult, equity premia represent a very interesting proposition. Historically, equity premia have been immune to the level of interest rates as well as to inflation surprises and all the while have delivered attractive and stable returns for investors. Their outstanding past performance is, based on our analysis, not due to the abnormal macro-economic environment, but rather to their diversification power that allow for the construction of portfolios with solid performance and risk management throughout market cycles. Furthermore, because risk premia have a low correlation with equity markets, they can provide a safer alternative to equity and bonds in periods when equity drawdowns are significant. In the current environment, this is an investment strategy that has and should certainly continue to attract the attention of risk-conscious investors.

Disclaimer

This marketing document has been issued by Bank Syz Ltd. It is not intended for distribution to, publication, provision or use by individuals or legal entities that are citizens of or reside in a state, country or jurisdiction in which applicable laws and regulations prohibit its distribution, publication, provision or use. It is not directed to any person or entity to whom it would be illegal to send such marketing material. This document is intended for informational purposes only and should not be construed as an offer, solicitation or recommendation for the subscription, purchase, sale or safekeeping of any security or financial instrument or for the engagement in any other transaction, as the provision of any investment advice or service, or as a contractual document. Nothing in this document constitutes an investment, legal, tax or accounting advice or a representation that any investment or strategy is suitable or appropriate for an investor's particular and individual circumstances, nor does it constitute a personalized investment advice for any investor. This document reflects the information, opinions and comments of Bank Syz Ltd. as of the date of its publication, which are subject to change without notice. The opinions and comments of the authors in this document reflect their current views and may not coincide with those of other Syz Group entities or third parties, which may have reached different conclusions. The market valuations, terms and calculations contained herein are estimates only. The information provided comes from sources deemed reliable, but Bank Syz Ltd. does not guarantee its completeness, accuracy, reliability and actuality. Past performance gives no indication of nor guarantees current or future results. Bank Syz Ltd. accepts no liability for any loss arising from the use of this document. (6)