The Japanese economy has marked the 60th consecutive month of economic recovery, the second longest period post WWII. Real GDP grew by 1.5% p.a. during that period. The profit level of all companies has largely exceeded the pre-GFC level, led by the domestic non-manufacturing sector. Companies have turned more positive towards hiring and capital investments.

Focus

Strong earnings momentum in Japan

Thursday, 02/01/2018The Japanese economy has marked the 60th consecutive month of economic recovery while the market stormed higher in 2017 supported by foreign investors, who re-entered aggressively in September, and the Bank of Japan doubling its ETF buying spree last summer. Participation in the labour market is growing and wage inflation is boosting consumer confidence, while business optimism is buoyant. These positives are finally gradually being reflected in the inflation figure and the consensus expects inflation to range between +0.8%/+1.1%, one of the highest levels in almost 25 years.

Joël Le Saux

Head of Japan Equities / Portfolio Manager

Yoko Otsuka

Analyst

“ In the current market environment, trying to time style and market cap rotation is highly risky. It is paramount to have a disciplined investment approach that focus on companies selling at discount to their fair value instead of chasing earnings momentum. ”

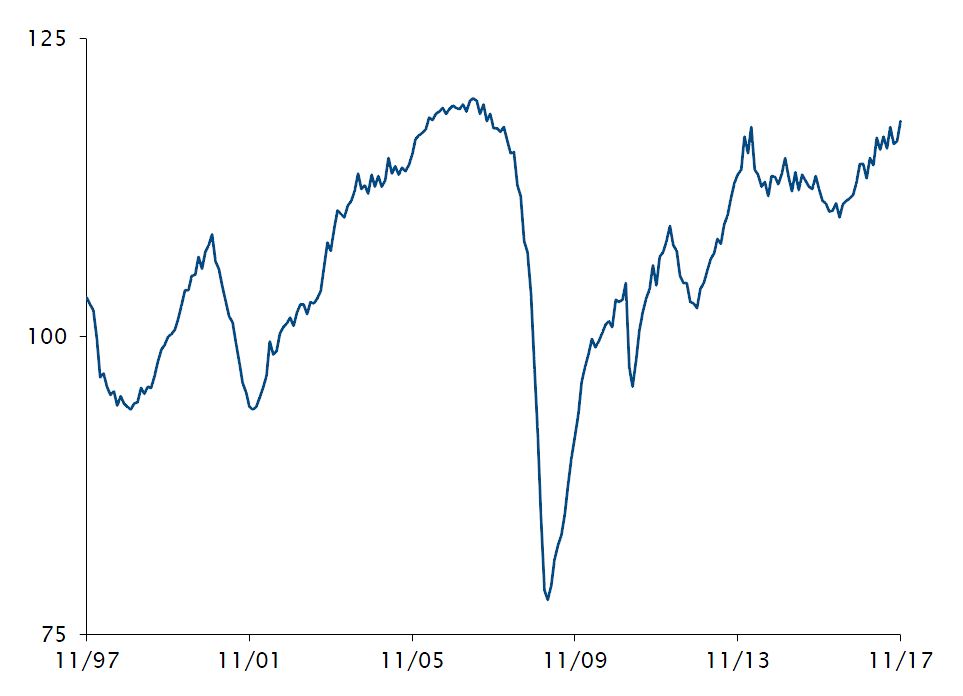

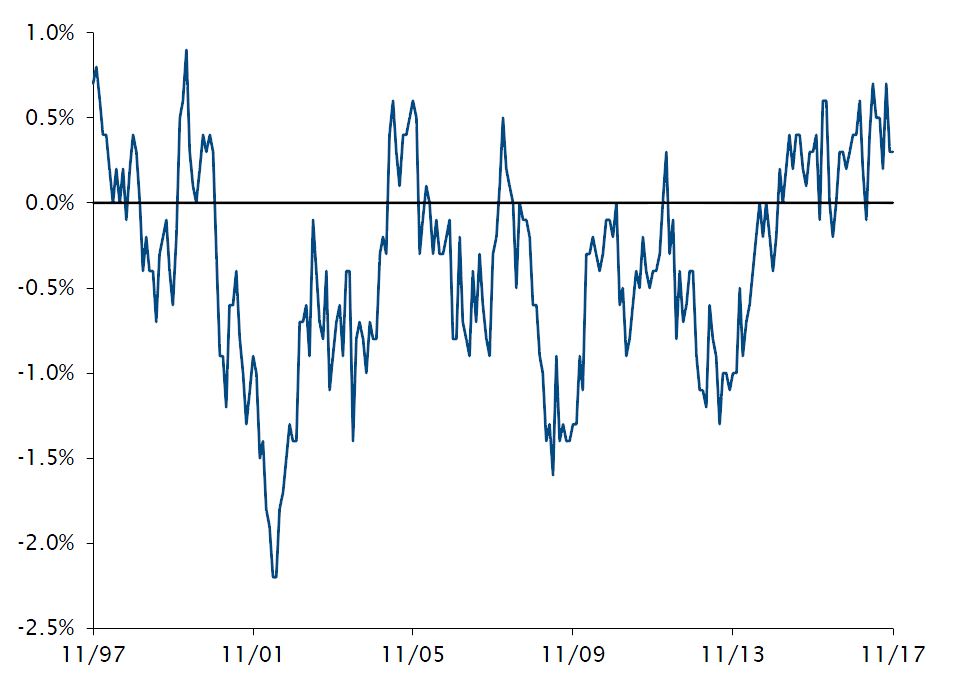

Economy under Abenomics

Business Cycle Indicators Coincident Index

Source

Economic and Social Research Institute. Data as at : 30 November 2017

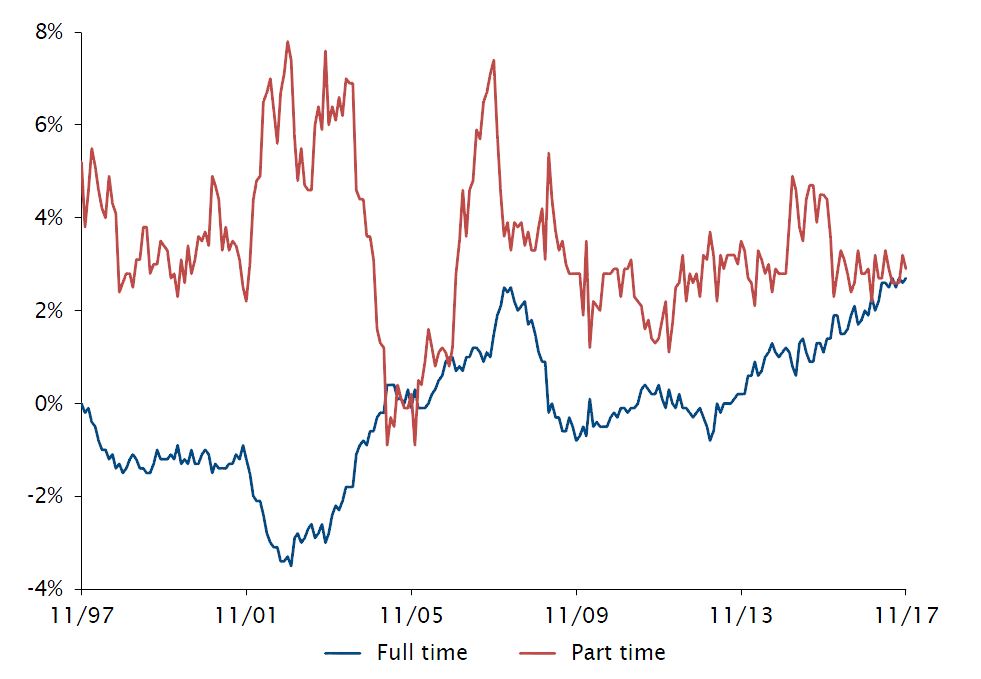

Currently, the job market is tight with a 2.7% jobless rate and a 1.6x jobs-to-applicant ratio, the best figure in the last 40 years. Due to a declining working age population by c. 1% p.a., female and active seniors joined the labour force recording a stunning +0.6% growth p.a. over the last 5 years. Also, the hourly wages for part time jobs have been increasing steadily around 2% p.a thanks to a structural supply-demand mismatch. Total compensation has reached 25-year high and demand of full-time workers is stronger than part-time workers. The consumer confidence that has recovered the pre-consumer tax hike level of April 2014 is likely to improve further through 2018 along with the favourable job market conditions.

Number of Employees All Industries YoY

Source

Ministry of Health, Labour and Welfare. Data as at : 30 November 2017

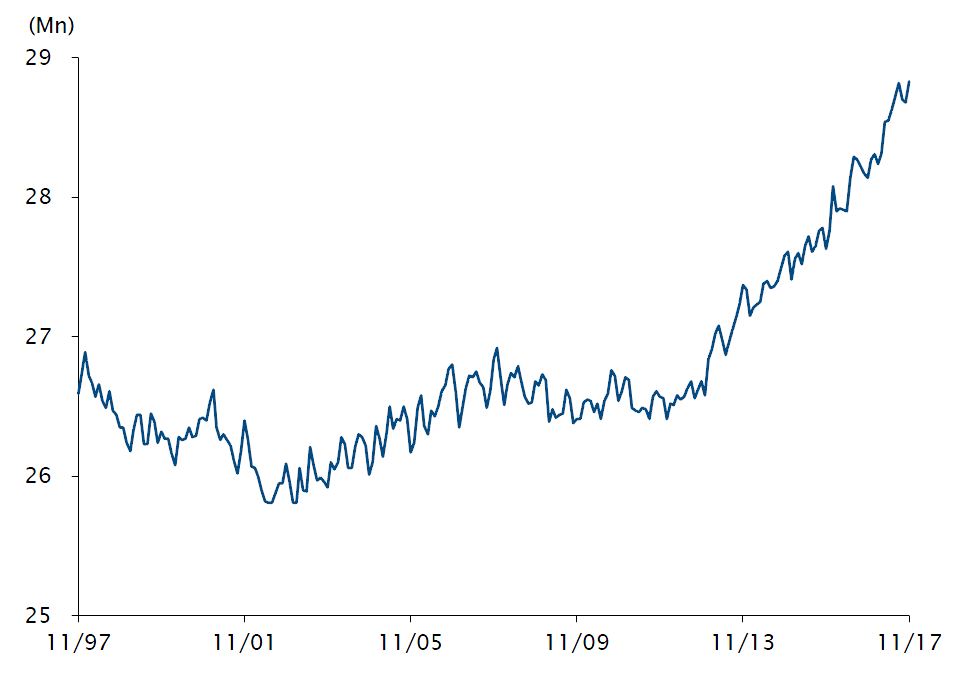

Female Labour Force Employed SA

Source

Statistics Bureau, Ministry of Internal Affairs and Communications. Data as at : 30 November 2017

Domestic capital investment has been positive over the last 5 years, especially from the manufacturing sector, seeing a strong need to upgrade/improve efficiency of their existing facilities. Although private domestic capital investment is still below the pre-GFC level, they are also investing overseas, spending in R&D and pursuing in M&As to make good use of their excessive cash.

Review of 2017

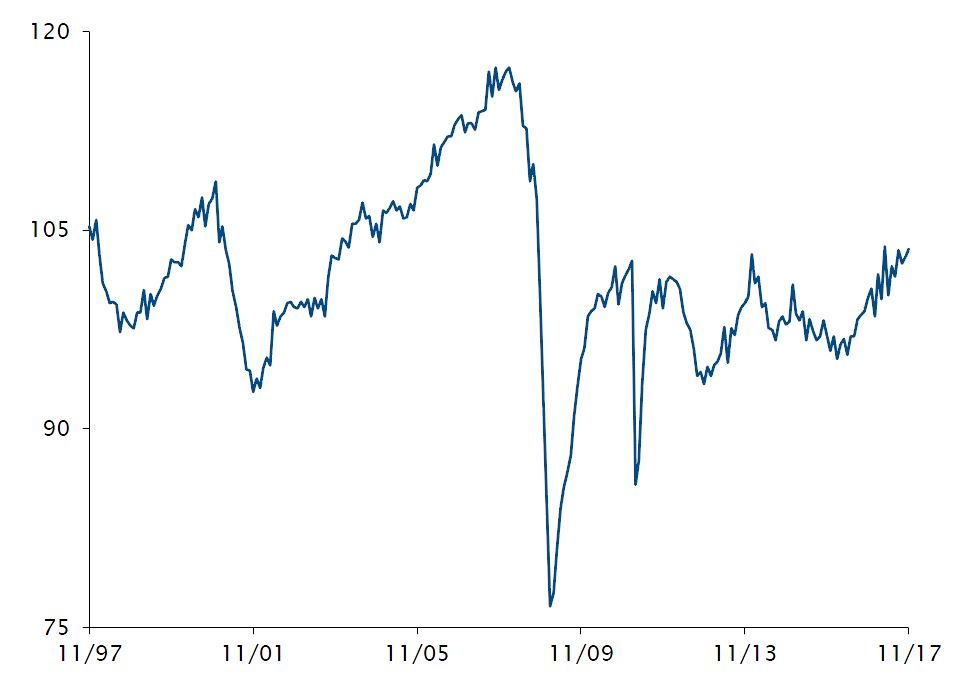

Last year was another good year for the domestic economy thanks to a strong tailwind from global cycle led by strong exports. The main beneficiaries have been tech and machineries, thus orders from China have been extremely strong, reaching the highest level ever. This has positively translated into the capital spending of manufacturers that is expected to increase by +17% yoy - exceeding their initial budget, rare for typically conservative Japan Inc. Finally, BoJ’s Tankan business conditions reached its highest level over 25 years in the last quarter of 2017.

These positives are finally gradually being reflected in the inflation figure with a headline CPI reading of +0.4% in 2017, basically the fifth consecutive positive reading. Even excluding the volatile components of fresh food and energy, the core CPI was up by +0.5% last year. For 2018 and 2019, the consensus expects inflation to range between +0.8%/+1.1%, one of the highest levels in almost 25 years.

Industrial Production SA (2010=100)

Source

Ministry of Economy Trade and Industry. Data as at : 30 November 2017

2018 onwards

The missing part had been the salary hike for full-time employees. The shift from regular workers to part-time workers that weighed on the average monthly scheduled cash earnings since 1996 is almost over. The salary increments of full time workers is set to contribute positively on the total average schedule cash earnings. This should result in higher spending by working households, which account for 70% of the private consumption.

Avg. Monthly Cash Earnings Scheduled YoY

Source

Ministry of Health, Labour and Welfare. Data as at : 30 November 2017

Monetary policy

In January 2013, the Bank of Japan set the "price stability target" at 2 percent and since then it has introduced a series of monetary policy; Quantitative and Qualitative Monetary Easing in April 2013, expanded it in October 2014, Negative Interest Rate in January 2016 and Yield Curve Control in September 2016. None of these policies have been effective to achieve its inflation target.

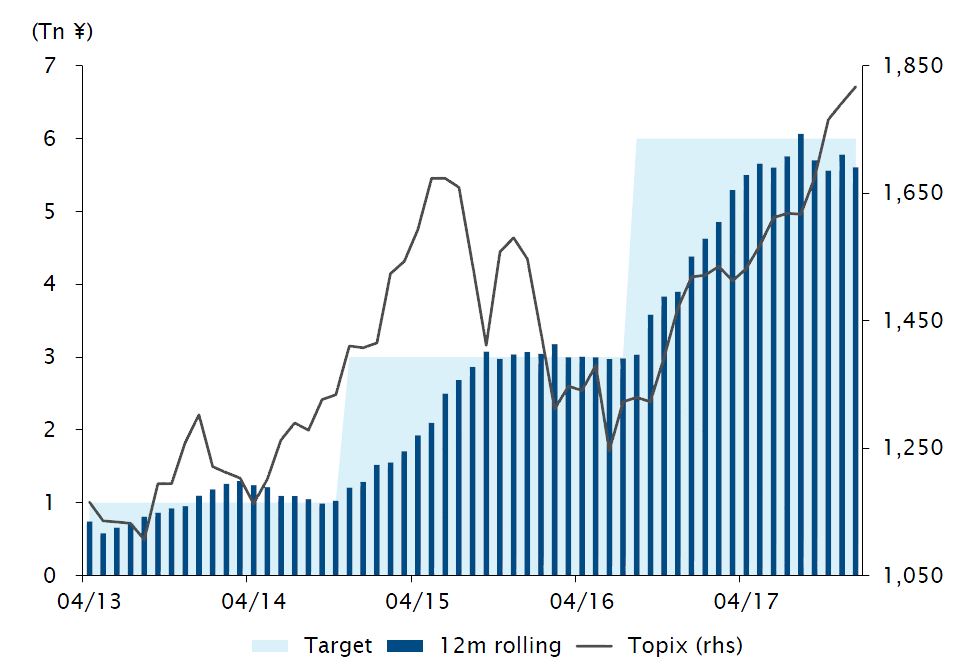

Running out of ammunition, 2017 was a quiet year with no official policy change. Focusing now on its YCC policy, the BoJ’s purchase of JGB diminished to around ¥60tn vs. target of ¥80tn. Triggered by this move, the market has recently started to discuss "stealth tapering", which is a move towards ending monetary easing without an official announcement. Meanwhile, the central bank was the largest buyer of the equity market throughout 2017. It introduced an ETF purchase programme in April 2013 as part of its QQE. In July 2016, it doubled its purchase target to ¥6tn p.a., c 1.5% of the market cap. Having an estimated ownership of 3%, the sustainability as well as the rational of this policy is today highly questionable.

ETF purchase & Topix

Source

SouBank of Japan, Bloomberg. Data as at : 31 December 2017

The current governor’s, tenure is set to end by March 2018. Most market watchers expect a reappointment for another 5-year term but the main focus for 2018 is whether or not there will be a change in monetary policy. If inflation trend stays on track, the government is likely to declare the economy officially "out of deflation" by mid-2018. Under such scenario, the central bank would take the opportunity to move towards ending monetary easing, which is important due to its decreased arsenal of monetary policy options, the expected impact of the consumption tax hike in October 2019 that could weigh on growth and the likely end of Fed’s tightening cycle by 2020 which could exacerbate the rate differential between the Fed and BoJ. We expect the termination of NIRP and an increase of the YCC target rate to come first, which is becoming the market consensus. Although the former will have a limited impact to domestic financial institutions, parallel upward shift of 5-10 years in JGB’s will have a large positive impact for domestic banks. In case of cut of ETF purchase programme, negative impact to equity markets is likely. Under any of these scenarios, it is difficult to envision a weaker yen vs. the US dollar over the medium term.

Market

Despite a stronger yen vs the US dollar, the Topix Net Total Return jumped by +22% in 2017 recording its sixth consecutive gain and its second best year since 2005. The market is now higher than in January 1989, year of accession to the throne of Emperor Akihito. Most investors remember the property crash that happened at the beginning of the Heisei era and the following 13-year long bear market.

Listed companies’ fundamentals are strong with both margins and profits at their peak. Basically, all companies are doing well but earnings have been especially strong in the sectors of IT, Materials and Industrials as of late helped by strong global and Chinese cycles.

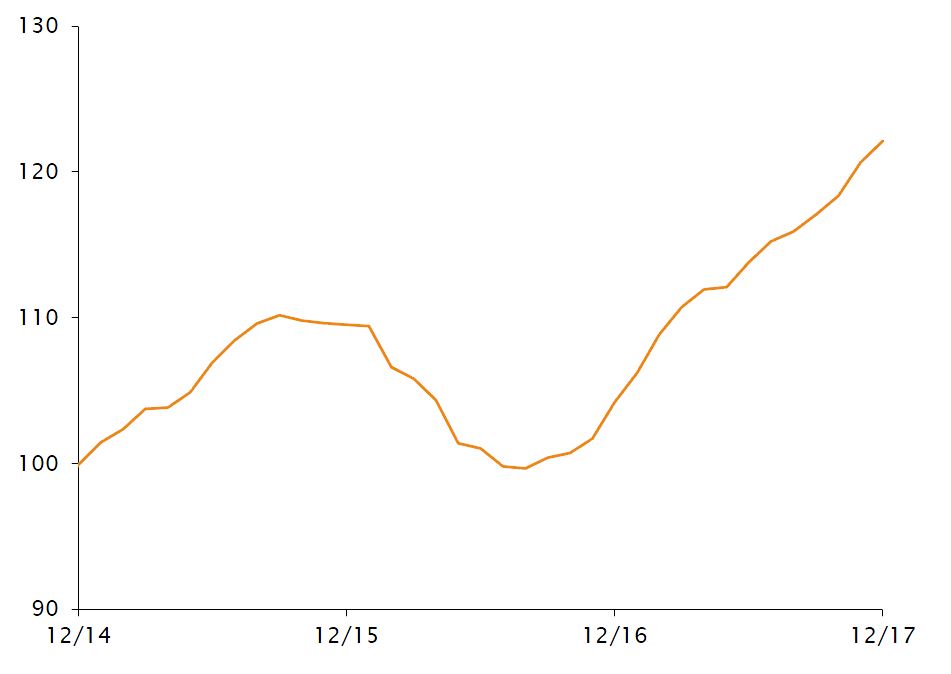

For the 17th consecutive month the consensus on 12-m forward earnings estimates has been revised upward. This is mainly due to good earning conditions in 2017 and forecasters not betting on an acceleration of growth in 2018. Their 8% EPS growth seems reasonable.

12m fwd EPS

Source

Bloomber. Data as at : 31 December 2017

TOPIX’ valuations expanded as a result of strong performance to 15x 12-m forward P/E near the highest level since the end of the GFC. The price to book ratio at 1.45x is also at a decade high. These metrics are fair in our opinion as the return on equity remains below 10%.

Higher than expected earnings could be achieved with a continuation of the strong global cycle and/or a further weakening of the yen vs. the US dollar but these factors would not mean higher valuations in our opinion. In order to achieve it in a sustainable manner, a structurally higher RoE is a must. Even though this would be reached with more leverage, most companies seem to be satisfied with their typical 40% shareholder return policy (dividends + share repurchases).

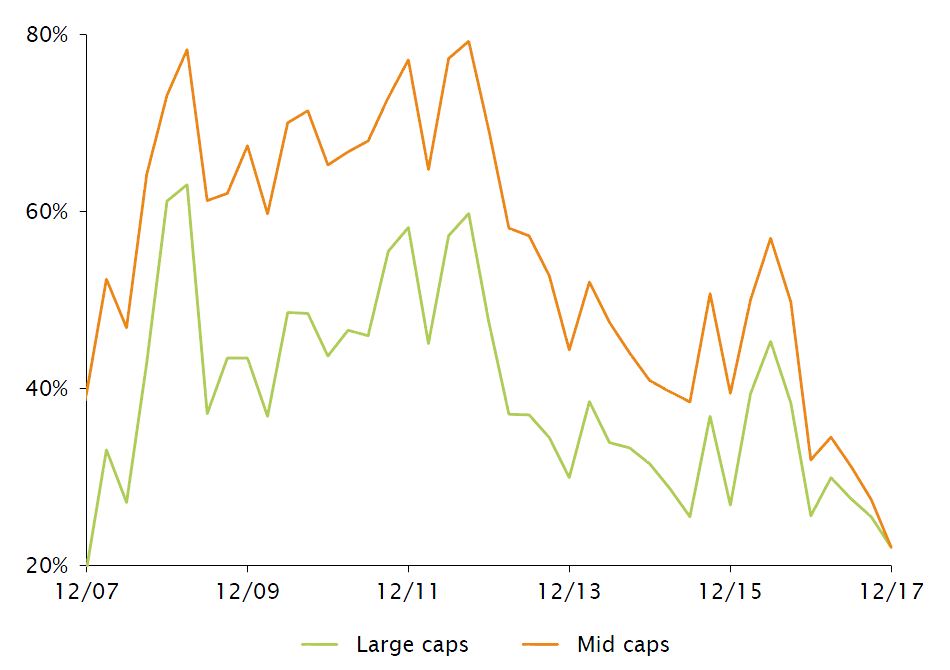

By market capitalization, the main feature since the end of GFC is the +235% rise of mid-caps, largely outpacing +172% and +126% for large and mega-caps respectively. Indeed, hidden mid-caps, a characteristic the Kabutocho, is not so anymore with basically none selling below book value and "rich" 16.4x 12-m fwd P/E.

Topix % of companies with P/B<1

Source

Bloomberg. Data as at : 31 December 2017

By sector/industry, valuation gaps of the four largest industries are extreme with cyclicals machinery and electronic components at 20x and 21x 12-m fwd P/E respectively while banks and automobiles at 11.4x and 10.5x. Mr. Market likes cyclicals currently.

Under these market circumstances, trying to time style and market cap rotation is highly risky. It is paramount in our opinion to have a disciplined investment approach that focus on companies selling at discount to their fair value instead of chasing earnings momentum. A balanced portfolio between mid-caps and large/mega caps is also wise considering the 12-year rally and high valuations of the former.

Disclaimer

This marketing document has been issued by Bank Syz Ltd. It is not intended for distribution to, publication, provision or use by individuals or legal entities that are citizens of or reside in a state, country or jurisdiction in which applicable laws and regulations prohibit its distribution, publication, provision or use. It is not directed to any person or entity to whom it would be illegal to send such marketing material. This document is intended for informational purposes only and should not be construed as an offer, solicitation or recommendation for the subscription, purchase, sale or safekeeping of any security or financial instrument or for the engagement in any other transaction, as the provision of any investment advice or service, or as a contractual document. Nothing in this document constitutes an investment, legal, tax or accounting advice or a representation that any investment or strategy is suitable or appropriate for an investor's particular and individual circumstances, nor does it constitute a personalized investment advice for any investor. This document reflects the information, opinions and comments of Bank Syz Ltd. as of the date of its publication, which are subject to change without notice. The opinions and comments of the authors in this document reflect their current views and may not coincide with those of other Syz Group entities or third parties, which may have reached different conclusions. The market valuations, terms and calculations contained herein are estimates only. The information provided comes from sources deemed reliable, but Bank Syz Ltd. does not guarantee its completeness, accuracy, reliability and actuality. Past performance gives no indication of nor guarantees current or future results. Bank Syz Ltd. accepts no liability for any loss arising from the use of this document. (6)