Although the skies seem to have cleared somewhat with regard to the economic outlook, the results of the Italian elections are, unfortunately, very difficult to predict because of a new electoral law that will be applied for the first time, and opinion polls whose credibility has been under severe scrutiny since a certain Brexit vote. In the following paragraphs, we will attempt to provide our readers with some clarification on the issues at stake in these Italian elections, to understand the forces at play, to find out whether any of the outcomes might be likely to disrupt or strengthen the structures in Europe, and finally, to discuss the possible impacts on the financial markets.

Focus

Parole, Parole, Parole…

Tuesday, 02/27/2018The Italian general elections will be held on the coming 4 March. They will elect the members of the Senate (315) and the Chamber of Deputies (620). The elections are the latest stage in a relatively busy European political calendar, beginning last year with the elections in the Netherlands, which were held in a far more uncertain environment both from a political and economic standpoint. France, Germany and Austria then followed suit with their own elections.

Fabrizio Quirighetti

Macroeconomic Strategist

A very uncertain issue

And doubly so... Firstly, because opinion polls do not show a clear majority for any of the major parties, whether that be the PD (Matteo Renzi's Democratic Party), whose popularity continues to unravel (receiving 25% of the votes), the M5S (Five Star Movement, founded by Beppe Grillo), with around 30%, and a centre-right coalition made up of Forza Italia (FI, led by Silvio Berlusconi), Lega Nord (LN, led by Matteo Salvini) and Fratelli d’Italia (FdI, led by Giorgia Meloni) with around 35% in total.

Secondly, these elections are governed by a new electoral law that was passed at the end of last year, known as the Rosatellum bis. This is a relatively complex system, which is designed to result in a majority government, either for one party or at least a coalition, as long as it comes well in front of the next in line (kind of a premium on the relative majority).

- Around 36% of the seats will be allocated on a first-past-the-post basis in one round (232 members of the Chamber of Deputies and 116 of the Senate).

- The rest of the seats, or around 2/3, will be allocated based on a proportional representation system, with a minimum threshold of 3% for individual parties and 10% for coalitions.

The main result will therefore be that coalitions are over-represented and the small parties will be under-represented. In order to have a majority in the new parliament, a coalition must obtain at least 40% of the national votes and around 70% of the single-member districts (first round only).

If we take a quick look at the possible scenarios/coalitions, at first glance it would seem impossible, despite the new electoral system, to achieve a sufficiently clear majority since there would have to be a very close-run race between the M5S and a centre-right LN/FI coalition, with both of these obtaining 30% of the vote, followed by the PD with 25%.

However, the centre-right coalition has the greatest chance of winning the majority in the new government. It would have to obtain 35% of the votes, vs. 25%-30% for the M5S, 25%-30% for the centre-left coalition (PD + a few other small parties) and 5%-10% for the extreme left (Liberi e Uguali, L&U).

Possible scenarios and implications for the markets

Let's start right away with the good news. A victory for Luigi di Maio, the designated candidate for the Five Star party, which would undoubtedly be the worst-case scenario for the equity markets, Italian bonds, and the single currency (given his ambiguous position vis-à-vis the European Union) seems highly improbable. This is particularly because his party does not want to form an alliance with the others, and they are not interested banding together with him either. Not only does he lack 7%-10% of the national votes, but, moreover, the centre-right is likely to grab the majority of the districts. In that event, and even with a victory for the M5S party, a minority government led by M5S has very little chance of seeing the light of day because the current electoral system favours coalitions, which would lead the President of the Republic to mandate a representative of the leading coalition (centre-right) rather than the leading party. That being the case, we can also dismiss the scenario of an anti-establishment government (M5S, FI and LN): even though it is possible in theory, given the scores achieved by each of these parties, in practice, there is a great deal of dissension between them and a reconciliation would lead to a loss of popular support because it would go against the very principles of M5S and its successful standpoint of “neither right, nor left”.

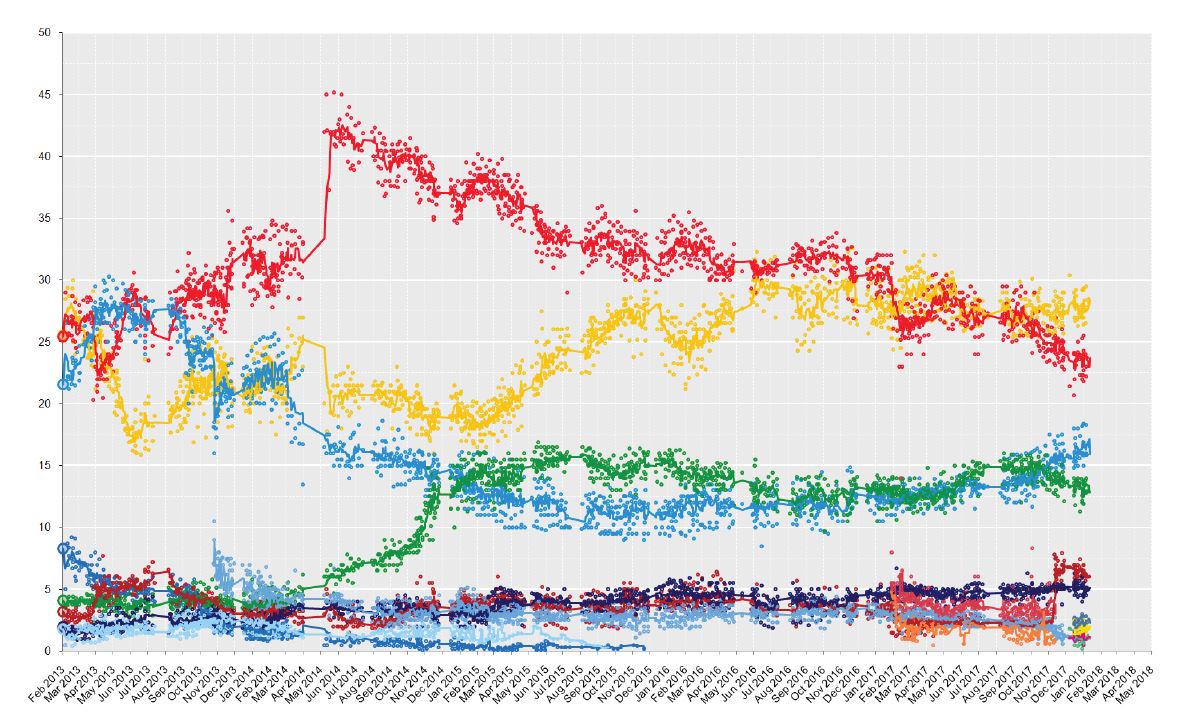

Results of opinion polls conducted since the previous elections on 25 February 2013

Source

Wikipedia. Data as at: 31 January 2018

The colour of each line corresponds to a political party

A centre-right government

According to the latest polls, this coalition is not far from obtaining a majority (it lacks between 20 and 50 seats). In the event that this shortfall drops to less than 20 seats, it could lead to the movement of some “centrist” parliamentarians from the left wing or desertion by other minor parties. This “small” majority would certainly be welcomed by an increase in Italian equities, or at least by an outperformance vs. other European markets, as well as a reduction in the spread between Italian and German bonds and a slight increase in the euro in the short term, because such a small majority would lead to instability.

The result would be an increase in uncertainty and tensions linked to the possibility of further elections in the next 6-12 months. However, beyond the positive impact of the news in the short term, there are unlikely to be any very significant or long-lasting effects because of a new uncertainty that would very quickly arise: the appointment of the new prime minister within this centre-right coalition! Silvio Berlusconi cannot take this on because he is ineligible as a result of legal proceedings in the past, but it is still he who calls the shots within his party; Matteo Salvini, and Lega Nord, have hinted at the desire to fulfil the role. The internal power struggle could be a lengthy and bitter one, potentially creating dissensions. As a result, this arrangement, which is not necessarily very stable, might not last very long.

Note that while Salvini's appointment at the head of the government would undoubtedly wipe out the positive reaction of the markets, an appointment from within the Forza Italia party would not guarantee an enthusiastic response from investors either. Particularly as the current prime minister, Paolo Gentiloni, who will continue at the helm during the transition period, is popular with investors.

A “narrow” defeat will not change much in terms of the scenario described above, apart from the following: the markets would not react so strongly in the short term and there would be less volatility in the medium term because the current prime minister will retain his mandate; there would also be fewer destructive internal power struggles and alliances within the centre-right coalition.

A government formed from a large coalition of centrists

This is a possible outcome in the event that none of the parties or coalitions obtain a clear majority. We would most likely see a slight negative reaction from the markets in the first instance, but not a sense of panic, since on the one hand Paolo Gentiloni would remain at the helm and, ultimately, if the centre-right and centre-left parties join forces, that would certainly be the best possible scenario. If the far-right parties, and the far-left parties to a lesser extent, were abandoned or marginalised, this would lead to a new wave of hope, similar to that witnessed after the victory of Emmanuel Macron's party in France. Here, too, we have to count on the movement of some parliamentarians to ensure the majority. And here, too, a large coalition does not necessarily mean a strong and cohesive one.

For the moment, the centre-right coalition seems to be the most likely outcome, but the possibility of a large coalition could very quickly become a real probability if the scores obtained by the far-right parties turn out to be lower than expected.

Further elections

If it proves impossible to form a government in the coming months, there will be further elections held 6-12 months from now, like those held in Spain in 2015-2016. The negative impact will be marginal but short-lived. The draft budget will be affected. But ultimately, would it be such a great surprise if Italy, which has had 62 governments since the end of WW2, does not have a proper government in place for a few months? Did Belgium or Spain, which have seen similar situations in the past, come out any the worse for wear? Maybe sometimes it's better to be ungoverned than badly governed. Italy is certainly not just any old economy in the eurozone. More than any other major eurozone country, Italy needs to put structural reforms in place to try and dilute, as quickly as possible, its dangerous cocktail of low growth and booming public debt. But most Italians are not fooled, since the worst-case scenario in terms of an explosion of public debt, namely a unilateral victory by Lega Nord, Liberi e Uguali, or the Five Star Movement, is not currently foreseeable. For the rest, the PD plans to maintain the status quo in terms of fiscal policy, and the impact of the Forza Italia plan is still difficult to evaluate (they promise significant tax reductions and an increase in pensions, although voluntary, or rather a desire to bring the primary surplus to +4% and reduce the public debt ratio to 110% in the next five years). Words, words, words... We can still dream, but the Italians do not believe that these measures will be implemented any time soon. Unless the winds of change one day blow over Italian politics, like they did in France.

Disclaimer

This marketing document has been issued by Bank Syz Ltd. It is not intended for distribution to, publication, provision or use by individuals or legal entities that are citizens of or reside in a state, country or jurisdiction in which applicable laws and regulations prohibit its distribution, publication, provision or use. It is not directed to any person or entity to whom it would be illegal to send such marketing material. This document is intended for informational purposes only and should not be construed as an offer, solicitation or recommendation for the subscription, purchase, sale or safekeeping of any security or financial instrument or for the engagement in any other transaction, as the provision of any investment advice or service, or as a contractual document. Nothing in this document constitutes an investment, legal, tax or accounting advice or a representation that any investment or strategy is suitable or appropriate for an investor's particular and individual circumstances, nor does it constitute a personalized investment advice for any investor. This document reflects the information, opinions and comments of Bank Syz Ltd. as of the date of its publication, which are subject to change without notice. The opinions and comments of the authors in this document reflect their current views and may not coincide with those of other Syz Group entities or third parties, which may have reached different conclusions. The market valuations, terms and calculations contained herein are estimates only. The information provided comes from sources deemed reliable, but Bank Syz Ltd. does not guarantee its completeness, accuracy, reliability and actuality. Past performance gives no indication of nor guarantees current or future results. Bank Syz Ltd. accepts no liability for any loss arising from the use of this document. (6)