So far, 2018 has presented investors with a number challenges that have threatened the near-decades long bull market. How will markets fare in the second half of 2018 and what does the global economy have in store for investors?

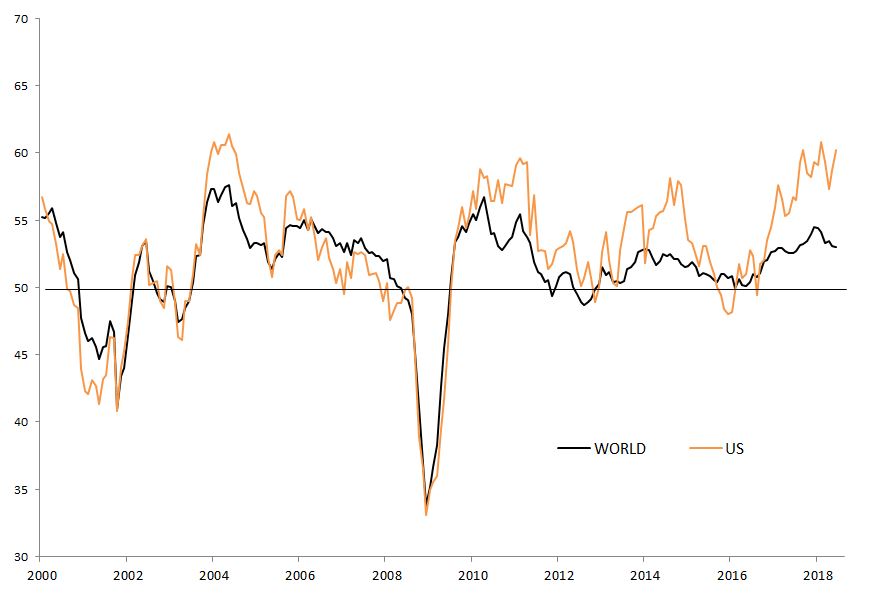

Positive growth, accommodative financial conditions and supportive sentiment point towards global growth, but with growing divergences between the U.S, Europe and the rest of the world.

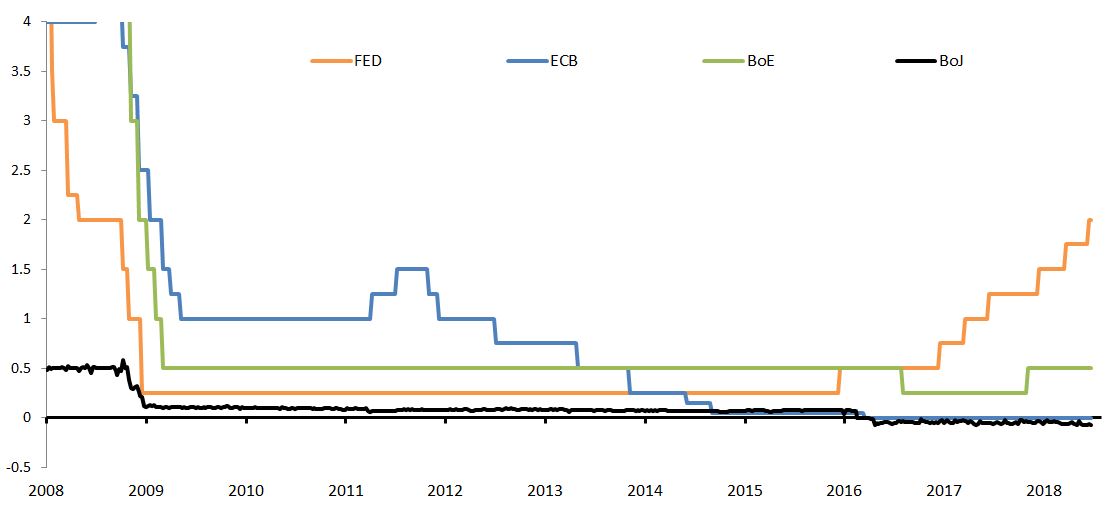

Inflation, currently not a material factor, will remain a focal point as it will shape monetary policy normalisation speed and magnitude going forward.

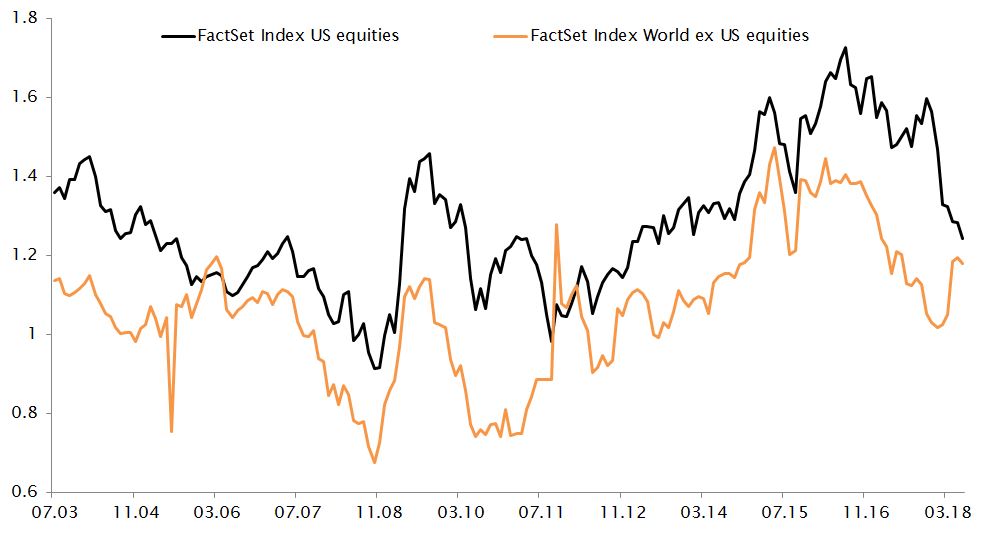

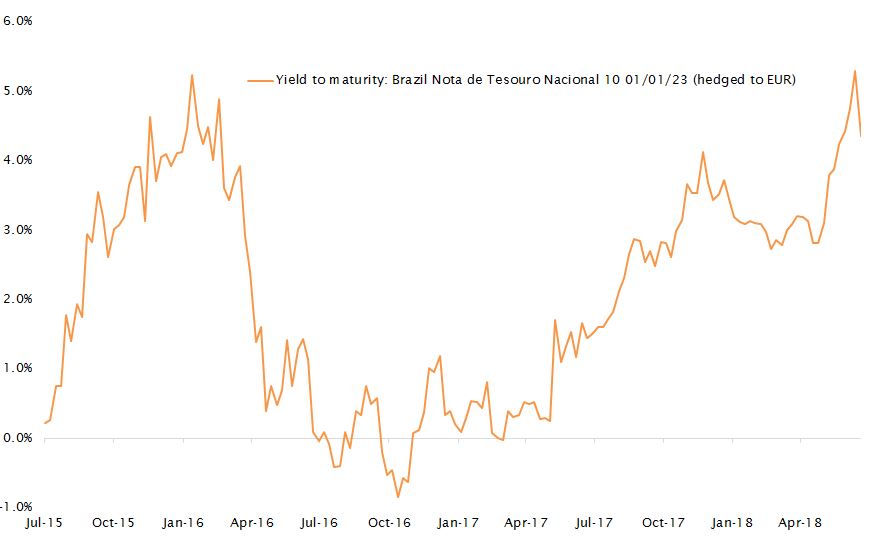

Asset prices are elevated, but pockets of value can be found. We favour U.S. Equities, U.S. Treasuries and selective Emerging Market bonds.